AKK Takes the Field: Oil Drilling Underway with Results Due in Weeks

Published 09-MAY-2016 10:50 A.M.

|

10 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

If Austin Exploration (ASX:AKK) was a person, its nickname would be ‘The Survivor’ for its ability to weather downturns, uncertain market conditions, setbacks and failed spuds.

Its CEO is famous for rolling up his sleeves and getting stuck in when required.

And the small, but dynamic management team are also rolling their sleeves up, conducting the drilling internally and saving shareholders a substantial amount of money by doing so.

VP/GM Colorado Mr. Aaron Goss, CEO Mr. Guy Goudy, Mr. Tim Hart COO

Suffice to say everyone at AKK has rolled up their sleeves over the past 3-4 months and got down to work, whilst also divesting several assets for a combined payback of $2.78MN.

It is now raising a further $1.7MN via a fully underwritten Rights Issue.

AKK has gone onto transform itself into a low-cost conventional driller with a strategy to enable it to stay profitable at below $40 a barrel.

This stock’s currently meagre $0.004 share price may not necessarily reflect this oiler’s true value.

That’s because AKK could be on the verge of a commercial oil discovery in the Pierre Shale in Colorado, one of America’s most prolific oil basins.

Drilling is currently underway and AKK expects to publish results in ‘late May’ – that’s just a few weeks away now.

Those results could serve as a catalyst that springboards the company to a new level – as long as AKK’s drilling comes in successfully.

However, bear in mind that this is a very small oil explorer and investment caution is advised if considering this stock for your portfolio.

The good news is that adjacent oil fields to AKK’s land are already producing thousands of barrels per day and preliminary indications suggest AKK may also be able to grab a slice of that oil-rich US mid-west pie.

Updating you on:

OTCMKTS:AUNXY

Austin Exploration (ASX:AKK; OTCMKT:AUNXY) has rejigged its oil game to best suit market conditions.

In an effort to boost its financial position and survive current oil market conditions, AKK has shed some weight and is planning to raise enough capital to assure its future security over the next 12 months.

Shedding weight

By that we mean AKK has divested its peripheral assets in Texas and Mississippi thereby bringing in a $2.78MN boost to its balance sheet.

The divestment means AKK has a smaller asset, yet high quality portfolio of oil and gas assets to manage and can therefore focus on establishing a small but vital foothold, hopefully in the form of regular cash flow.

The added benefits are that AKK is now debt-free and is only involved in projects where it has 100% ownership.

Given current low oil prices, this is important because being debt-free removes the possibility of negative equity. Meanwhile working only on assets it operates, AKK can retain full control over future expenditure and project planning.

If oil prices recover, AKK will again look to pursue its more exotic oil licenses, but for the time being, it’s all about consolidating, staying afloat and offering a clear path of growth and upside for its shareholders.

Funds for drilling

Any oiler working hard to make ends meet needs funding.

AKK is raising $1.73MN from a fully underwritten Rights Issue .

Both the divestments and Rights Issue are steps to secure AKK’s future in terms of lowering costs and raising the probability of revenues.

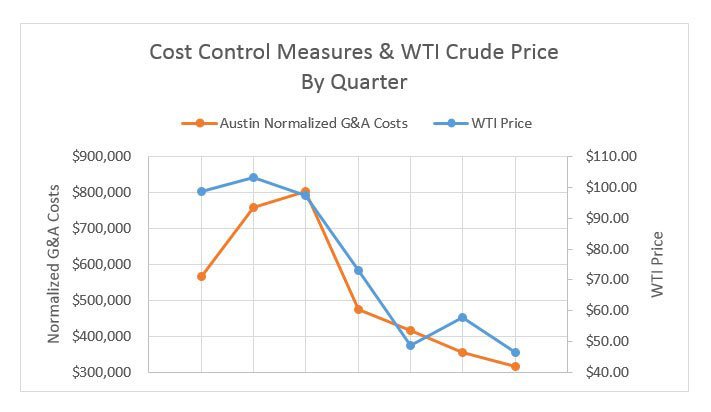

This is how the streamlining at AKK looks like on a chart:

AKK’s cost base has been significantly lowered alongside falling oil prices while its general and administrative expenses (G&A) have been slashed by 75% .

This is the kind of plan we like to see here at The Next Oil Rush : oilers being pragmatic and realistic about their abilities given market forces at play out of their control.

AKK cannot adequately progress its entire gamut of projects despite all of them being excellent assets at higher oil prices.

But if it focuses on just two (Colorado and Kentucky), it can realistically expect to get its overall cost structure low enough to make its oil production economically viable at ~$40 per barrel.

With funding secured, the leaner and meaner AKK has eyes only for one thing: drilling a well and proving up a commercial oil discovery in Pierre Shale formation in the DJ Basin.

Let’s take a look at how AKK is going about it

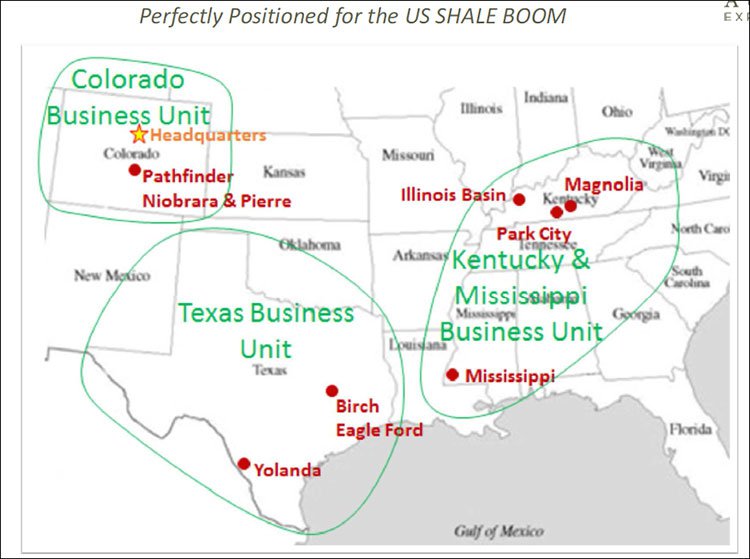

AKK is now squarely focused on its Colorado and Kentucky prospects given their larger size and AKK acting as operator on both.

Colorado

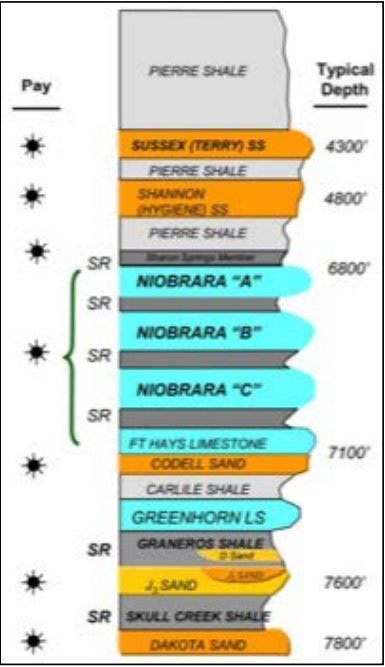

According to AKK’s reserves report, its Colorado asset has a p90 contingent resource of 15.4 million barrels of oil to a p10 resource of 26.6MMbbls, and that’s only in one formation. It successfully proved the Niobrara formation by drilling the first productive horizontal well in the Florence oil field.

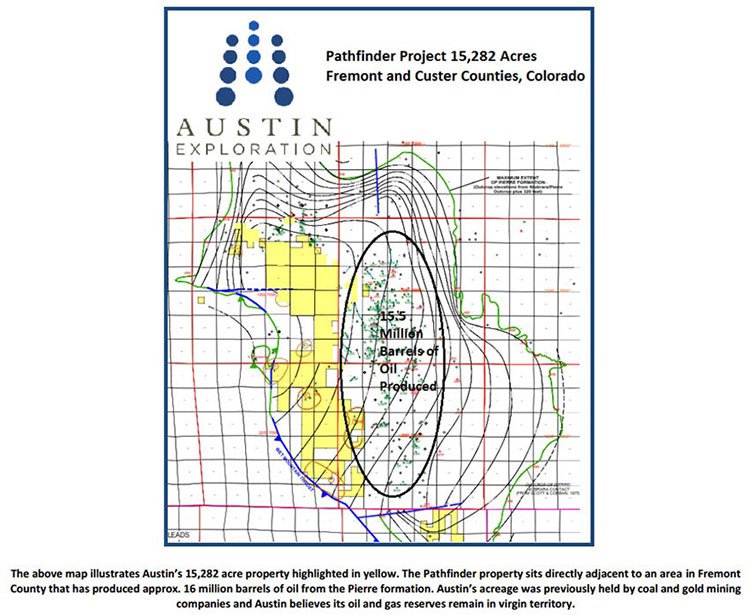

AKK plans to complete a reserves study on the Pierre post drilling which should provide a significant boost to the oil in place in its’s 15,282acre project – remember more than 15 million barrels of crude oil has been produced ACROSS THE ROAD from Austin’s property in the ire formation.

More information as to the success of C18#2 will be made available later this month, and could breathe new life into AKK’s share price.

It all just depends on how much AKK can prove up and what depth as this will directly affect how cheaply it can be accessed and extracted.

The property consists of 15,282 acres lying over the DJ Basin (one of North America’s most prolific oil and gas producing basins), and is large enough to accommodate more than 350 wells in the Pierre formation.

A commercial discovery would position AKK as one of the lowest cost oil producers in a depressed market.

The ‘nearology’ factor

One factor AKK has in spades is the nearology effect.

If your neighbour has millions of barrels of oil, there is a tendency to raise your own chances of proving up something similar.

Immediately to the east of AKK’s Pathfinder region is a project where 15.5 million barrels of oil have been produced so far.

ASX-listed Comet Ridge Energy (ASX:COI) with its market cap of $30.5M, has been at the forefront of this drilling, having drilled 25 wells at the project from 2008 to 2012.

Of the 25 wells drilled, 22 went on to become producers with the daily production from these wells reaching averaged 35,000 barrels of oil per well produced so far.

The estimated recoverable reserves from this field have been put at 75,000 barrels per well, a demonstration of the scale AKK could be looking at.

The 30-day average initial production figure from the Comet Ridge wells was 116 barrels of oil, with over 190,000 barrels of oil produced at the project from the Pierre shale (and still counting).

However, the best well had a 30-day initial production rate of 360 barrels of oil per day, meaning pay back of less than 45 days.

As you can see from the picture below, Comet Ridge’s former project is right next door to AKK’s land (shown in yellow).

One more factor in AKK’s favour is its tidy deal with Math Energy Drilling – that secures exclusive access to top notch drilling equipment at a low cost for at least 12 months

It just so happens that AKK’s Non-Executive Chairman has a stake in Math Energy and thereby can arrange for a discount, or two.

COO Mr. Tim Hart, Chairman Dr Wm. Mark Hart, VP/GM Mr. Aaron Goss

The deal also means AKK can drill its next well for under US$500,000 – a significant discount to the industry average of around US$700,000-$1MN per well.

Professional advice should be sought if considering these numbers as part of your investment decision along with other investment factors related to this stock.

The state-of-the-art rig is currently onsite and working overtime to get AKK a catalyst to present to shareholders.

Here’s COO Tim Hart operating the Drill rig...

An oil quagmire for some, reaps opportunity for others

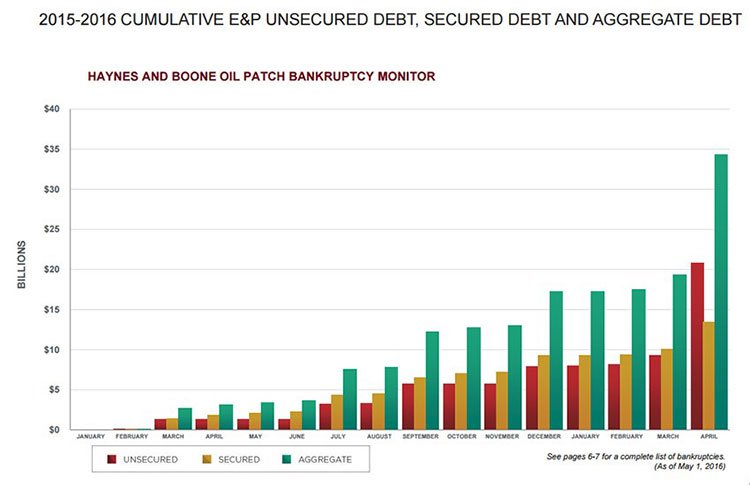

The ongoing oil downturn is so severe that almost 70 US oil & gas companies have sought bankruptcy in 2015-2016 alone.

Reams of oilers have bitten off way more than they can chew in the good days, and are therefore forced into bankruptcy, unable to stay economically viable at <$40 per barrel as the bad times rolled in.

Here’s what all those bankruptcies mean for debt – as you can see, bad debts are growing and now stand at almost $35BN. Remember, this is just the US and doesn’t include oilers from other countries.

The reason this factor is an important one for AKK, because the company is determined to win in the game of ‘Survival of the Fittest’, currently being played by US oilers.

If more bankruptcies are processed, it’s likely to translate into lower oil supply and may help prices recover.

The key is to stay in the game long enough to see higher oil prices. Most oilers will not make it, but the more efficient and prudent ones likely will.

The end result is that once oil prices find a new equilibrium, the oil market is likely to have only the strongest and most cost-effective producers left behind.

That’s exactly where AKK wants to be at some stage in the coming months and years.

The telecom and energy boom-and-bust cycles have notable parallels.

Pioneering technology brought an influx of investment to both industries, a plethora of new, small companies issued high levels of debt, and a subsequent supply glut hit prices hard just as demand fell sharply.

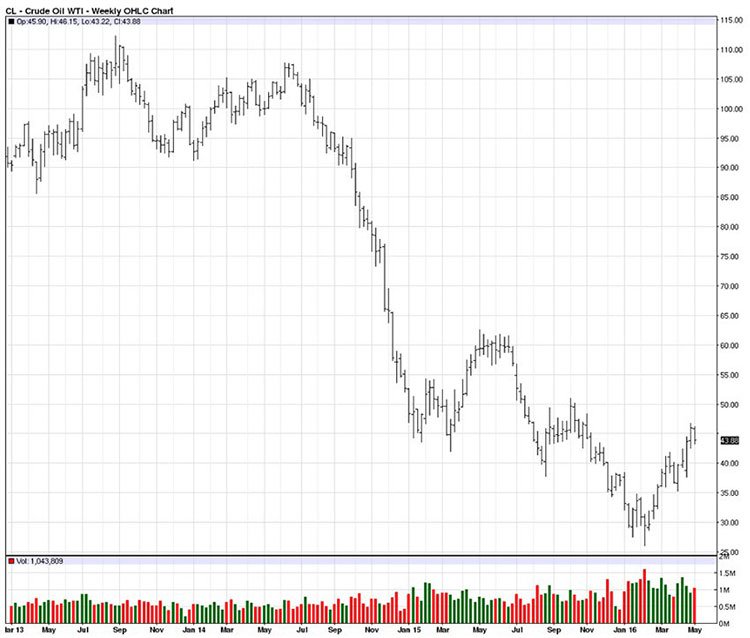

Oil prices have been on a downward trend since 2014, but there is some hope that the recent bounce from record lows around $30pb will continue beyond the current $43pb price, oil’s highest since November 2015.

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance.

As oil prices have trended lower, average daily trading volumes have risen. This could be an indicator that at around $30-$40 there is a strong base of demand and therefore could be a floor for oil prices moving forward...

However trying to guess the oil price is not easy – an investment should not be made on speculation on energy prices alone. Always take into consideration your own personal circumstances before choosing to invest in a stock like AKK.

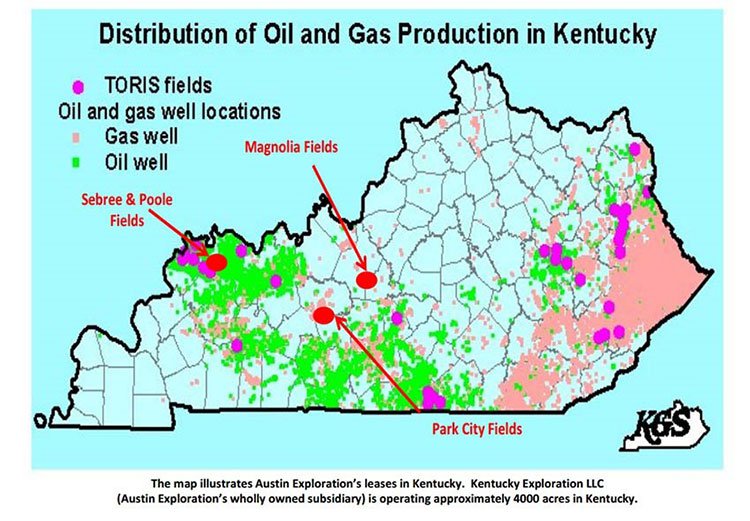

Not forgetting Kentucky

With its Pathfinder project in Colorado moving along nicely, AKK’s other asset it thinks could go commercial in the coming months is based in Kentucky.

In Kentucky, AKK is operating a 4000 acre asset in the Illinois basin, on a 50/50 joint-venture (JV) basis with a private Australian investment company.

Word is that the Illinois Basin could be the next Bakken and AKK is thus determined to maintain property in this region as it views the region as having excellent upside potential.

Here too AKK is applying its cost-saving mantra to weather the oil downturn.

Leases with high operational expense and high water haulage, electricity consumption and chemicals usage have been put on hold until oil prices start to recover.

While the oil market works out its supply and demand imbalances, AKK as pursuing low cost, shallow (~4,000ft), high impact drilling to establish a low-risk, low-volume production schedule.

Here again, AKK aims to haul in cash flow and retain its licenses with a view of future expansion subject to market conditions.

Here’s the lay of the land in Kentucky with AKK’s leases shown and labelled in red.

Be greedy when others are fearful, and be fearful when others are greedy

Famous words from Warren Buffet, that currently mean a great deal in oil.

The oil market is undergoing a historic cull whereby any oilers that missed a beat in the good days between 2010-2014, are now paying the price of being lumbered with expensive assets that are not commercially viable.

As a junior oil explorer, AKK is in a comparatively better position than most other US-based oil companies because its assets are debt free, there is funding available for more exploration and its overall cost structure is rather peer-beating when you look at the amount of bankruptcies sprouting in the US.

The Colorado Oil and Gas Association has put the overall oil potential of the Niobrara Shale at 2 billion barrels of oil which AKK will eventually explore as and when conditions improve.

The long-term blue-sky potential for AKK is that will be able to drill into the three individual zones of the prolific Niobrara Shale, found at greater depths around 6800-7100ft.

AKK is a survivor by nature so its current gauntlet only serves to make this plucky explorer even more battle-hardened.

There could be light at the end of the tunnel for AKK with its Colorado drilling results due in the coming weeks.

Can AKK can strike a decent hit and prove up enough oil to set the stock on a commercial future it has always planned for?

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.