Large Perth Basin Holding for Micro Cap ASX Stock: M&A Appeal?

Published 26-OCT-2016 10:42 A.M.

|

13 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Welcome to the Wild West, a land rich in entrepreneurship and natural resources where many a gas or oil company has come to test their luck.

Like any good Western, there are the lily-livers who never try, the losers who end up left (literally) in the dust, and the hero who braves a new frontier right on the border of civilisation and the wilderness.

Today’s ASX micro cap company is posturing to be the hero.

That’s the plan, anyway.

While pretty much all oil and gas plays have an element of ‘wild card’ about them, the closer they are to historic discoveries, the more it becomes a matter of strategy over dumb luck.

That’s where the difference lies for today’s company, who have secured very reasonably priced permits in known hydrocarbon systems within the onshore Perth Basin – an area running 1300km along the south-western coast from Geraldton to Augusta in WA, which holds numerous currently producing gas developments and a number of new gas discoveries.

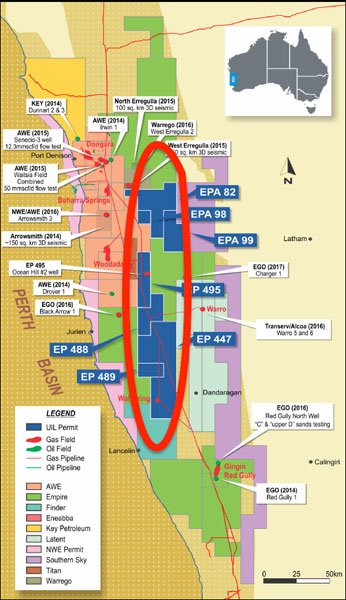

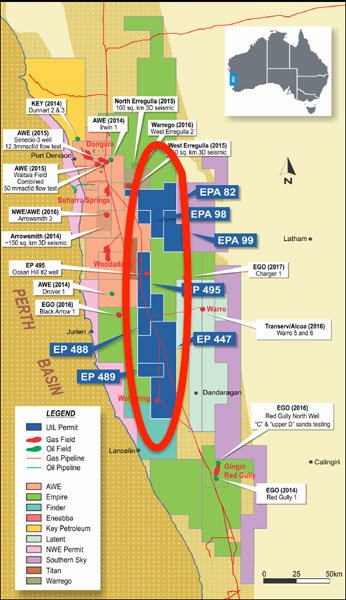

Following a recent transaction, this $8M capped ASX stock owns 100% of one of the largest contiguous holdings in the Perth Basin.

Despite the proven presence of those hydrocarbon systems, the entire Perth Basin is still considered relatively underexplored with only about 350 wells drilled to date.

There’s certainly scope for much bigger game changing discoveries here, and with a host of explorers undertaking exploration, and a state government looking for more gas, it’s quite a fertile environment to be in for a micro cap stock.

As part of a recent deal, this company has secured the Ocean Hill gas discovery, an independently certified contingent (2C) resource of 360 bcf.

Furthermore, its southern Perth Basin permits hold prospective resources of 328 bcf (best estimate), including an abandoned well that flowed at 0.6 mmcfd.

In short, what could be attractive to investors here is the size of its acreage and its position, which means any future gas production can be marketed to undersupplied domestic users... and through existing and planned LNG export facilities.

The size of this company’s assets could also be of interest to major oil and gas players, who are looking for proximity to infrastructure and faster, cheaper paths to commercialisation. A buy-out or farm-in is not out of the question if this company lines up all its ducks.

As an early stage play there is no guarantee of a buyout or acquisition occurring, so investors should tread a cautions path to an investment decision and seek professional financial advice for further information.

The good news is this company has already signed a conditional agreement for a private company to farm-in on its Walyering project within its Perth Basin permit EP447.

The company’s speed to commercialisation may also be helped by current market conditions including regulatory changes in WA. The state of WA is currently going through significant legislative and structural changes as far as gas is concerned, and is putting its contracts up for renewal as soon as 2020.

An onshore gas flow like this company is aiming for will offer a more cost-effective solution to the lower-priced domestic market and there’s no doubt that there are deals to be had.

You just have to look at its nearology to other players in the region to realise that there are substantial deals to be done.

The bigger question is, are there gas discoveries to be made?

The company will soon find out, as it is gearing up for drilling in 2017, but will need to either farm out or raise further capital to do this.

Led by an MD that previously took a small cap company from a $50M valuation to $500M, this company certainly thinks there is more value to be extracted from the Perth Basin and now could be the best time to develop plans while opportunities are still cheap.

Introducing:

![]()

UIL Energy Ltd (ASX:UIL) has put together a game plan which could help resuscitate the domgas (domestic gas) market in WA.

In February UIL agreed to binding terms with Eneabba Gas, resulting in an important gain – UIL now owns 100% of the Ocean Hill gas discovery, which has independently certified 2C contingent resources estimated at 360bcf.

The company is currently offering an SPP to existing shareholders to raise up to $750,000 , at 5 cents per share – with the application period set to close on 7 November.

UIL has already raised $750,000 through a placement to professional and sophisticated investors through the issue of 15 million new shares at 5 cents per share.

The total $1.5M capital raised will go towards progressing its the Perth Basin assets, in particular the funds will progress with the Ocean Hill 3D seismic and drilling approvals.

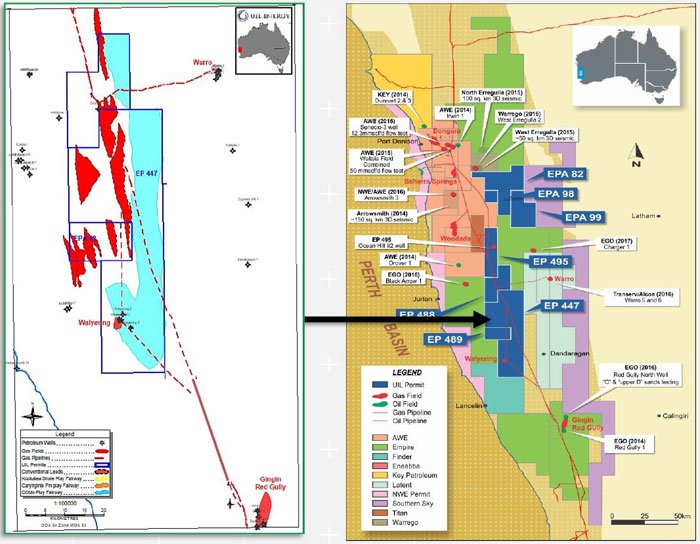

The funds will also go towards 3D seismic, the Walyering farm-out with Bombora Natural Energy , and upgrading prospects on its central permits (see map below for a detailed look at its Perth basin portfolio.

UIL has signed a conditional agreement to enable Bombora to farm-in on the Walyering project area within UIL’s Perth Basin permit EP447. Bombora is to fund $2.5M for maximum 100km 2 3D seismic survey and earn a 70% working interest in four granular blocks.

First let’s take a look at Ocean Hill.

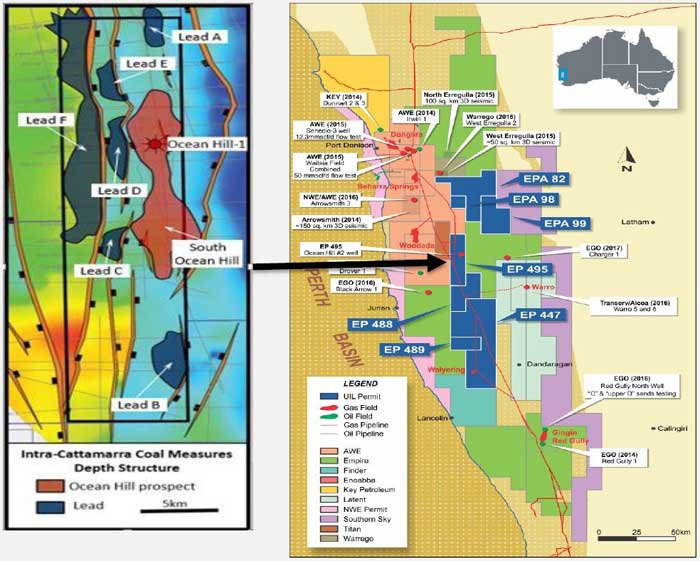

Ocean Hill’s original gas discovery was via the Ocean Hill-1 well drilled in 1991, which recorded over 800m of gas shows, with potentially 100m of net pay.

Testing delivered a combined flow rate of 0.7 mmcfd with 17 bcpd, indicating this could end up being something much more substantial.

The nearly 300km area has a best estimate 2C contingent resource of 360 bcf of gas – and its now all UIL’s. Over the medium term, UIL is looking to drill again here, and see if it can expand on the Ocean Hill-1 results.

Since Ocean Hill-1, further development and exploration of the same area is now made much easier thanks to advancements in technology such as 3D seismic mapping, which UIL plan to fully exploit in the near term.

As with any gas exploration venture, it is the financing requirements that tend to hold things up. That’s about all that stands in the way of this company and realising more value in its assets.

The large size of the acreage – one of the largest contiguous holdings in the Perth Basin area – could be attractive to larger companies, and there is already news of farm-ins ( 4 blocks by Bombora in the South of UIL’s zone ), and even third parties interested in funding earn-in work programs.

You’ve also got privately owned Warrego Energy drilling in the North which will help cover ground in terms of exploration.

Given the need for capital to fund evaluation and development activities that always precede commercialisation in these sorts of deals, UIL will be searching for a partner. In general, gas buyers are progressively becoming involved higher upstream as partners, so this is a definite possibility for UIL.

Of course, confirming a farm-in partner is no guarantee for UIL, and like all small oil and gas stocks, there is no absolute guarantee that an investment will turn out to be a success, so invest with caution.

Questions around financing will be also be indicated by the timing around the company opening a data room. For those that were unaware, many companies use data rooms to coordinate discussions between potential investors, partners and to attract new capital.

Confidential documents like non-finalised contracts, site photos and engineering sketches can be shared in a secure way across internal and external stakeholders (board, bidders, lawyers, investors) through a data room.

When this happens, you’ll know a company is gearing up to secure funding partners.

Whilst it is early days for UIL, developing onshore plays does cost less than offshore options, so a nice onshore discovery will pose an attractive alternative in terms of what UIL can bring to the table regarding gas supply.

With much of the recent media hype focusing on domgas in Australia’s east coast markets, WA opportunities (and concerns) have certainly slipped somewhat under the radar...

... with the exception of forward-looking companies checking out the commercial potential across the other side of the country, such as UIL.

Whatever way you look at it, there’s definite potential here.

The Perth Basin has attractive projects given past drilling success, existing infrastructure and the fact gas prices are no longer linked to oil, particularly in the domestic market.

The pipelines cutting directly through UIL’s acreage are a big boon for the company, too...

Where exactly is UIL going?

On the north border of UIL’s permit zone is Scottish company Warrego who also have permits in the Perth Basin.

Warrego’s drilling, adjacent to UIL’s northern permits, will commence in 2017, taking on some of the exploration and allowing UIL to focus more on their southern prospects.

Based upon recently completed 3D seismic, Warrego is drilling on the north border of their permit zone (within 5kms in fact!), and any positive results from this or future drilling will likely have an impact on the inherent value of UIL’s permits.

UIL has three permits adjacent to Warrego’s owned Erregulla field where Warrego’s scheduled drilling is set to commence.

Let’s zoom in on the map again and take a closer at this company’s positioning.

The north-western flank of permits held by UIL have potential for key reservoir intervals similar to AWE’s highly valued Waitsia discovery.

In the centre we have the Ocean Hill project as shown below.

Funds raised from UIL’s current SPP will be used to progress the development in this highly prospective area with a 3D seismic programme and drilling approvals focused on Ocean Hill, as well as in the North.

Ocean Hill has proven gas productive zones in the Jurassic (Cattamarra Coal Measures) similar to the Red Gully Gas Field. Its first discovery flowed at 700,000 scf/d.

Now UIL have begun preparation for a 3D seismic mapping in the northern areas aimed at high grading identified prospects.

In the South of UIL’s permit zone is the Walyering project area, partly funded via the Bombora farm-in, which crosses four blocks into the EP 447 permit.

A few points to consider

There are a couple of factors here that might prick the ears of gas and oil investors looking for a potential 10-bagger.

At the same time, investors should not assume that an investment in UIL is guaranteed to be successful, and caution should be applied before making an investment decision in an early stage stock such as this one.

UIL is looking to conduct early 3D seismic mapping to shore up its drill targets, and also enter into joint venture deals to bring it all to commercialisation.

Assuming all goes well with its plans for the next 18 months, it could be very well placed to piggyback off the groundwork of previous companies.

Demand and supply curves are starting to move in favour of higher gas prices domestically, over the long-term. Domgas supply is set to fall when current contracts expire in 2020.

As WA’s gas prices aren’t closely linked to the (fallen) global oil price curve, that could equal high margins for the companies controlling permits onshore.

UIL is quietly confident about the prospectivity of its permit zones – and the potential success of their plans for conventional and unconventional mining ventures.

In the long-term, global demand for natural gas is strong. It is anticipated that the role of natural gas will play a key role as countries transition to lower-carbon energy solutions in response to climate change.

So while oil and gas plays are always a volatile proposition, choosing gas might mitigate at least some risk.

All tomorrow’s parties...

UIL have a few key reasons for an optimistic outlook at the moment.

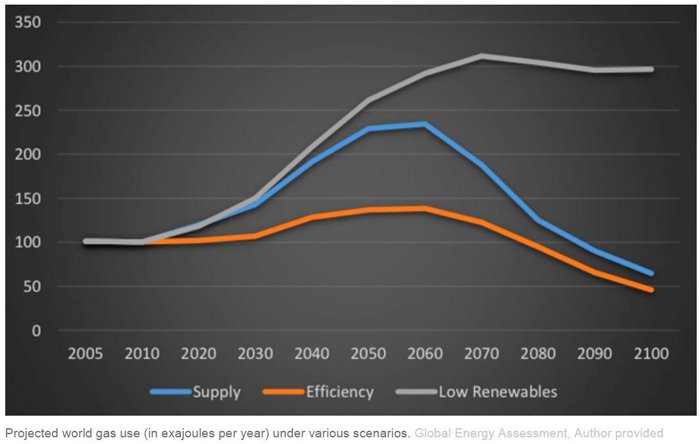

Data from the Global Energy Assessment predicts that global demand for natural gas will go up in all scenarios until at least 2050.

That’s a pretty good start for a gas explorer.

There are a number of other external and internal events, too, which are looking to conspire in favour of UIL in the coming 12 months.

Origin Energy Perth Basin asset sale to provide look through value for UIL

Origin Energy is looking to balance its books by completing a significant asset sell off, and that includes its ventures in the Perth Basin. Whatever Origin can get for its assets will give UIL a much better indication of what it is sitting on.

The energy giant intends to generate at least $800M through asset divestment, including pipelines and non-operated upstream interests.

Origin has stated reasons for this divestment relating to the fall in global oil prices, as well as an increasing commitment to reduce carbon emissions. Its current divestment sits at around half its intended total having sold Mortlake Pipeline and Terminal Station, so there’s more of the same to come before their divestment process ends towards the latter part of next year ... so keep an eye out for any Perth Basin asset sales, as it will provide a good indication of the look through value of UIL’s assets.

Sizing up the talent...

UIL Managing Director John De Stefani was formerly CEO of Bow Energy Ltd during a growth phase that took the company from $50M to $550M.

This indicates he has the experience to lead a micro cap stock to a much, much larger valuation – we are hoping he can do something similar with UIL.

Prior to Bow, he has worked as Director of a power generation business, and has nearly a decade of international energy experience spanning projects in the US, UK, Egypt, Turkey and the Philippines.

Executive Chairman Simon Hickey is the founder of UIL – he has more than 20 years of experience in the resources industry and has been a director of several ASX and TSX listed companies.

Also adding to the sizeable pool of resource industry expertise is non-executive director Garry Marsden, a petroleum geologist who has held positions with Pancontinental Petroleum, Bankers Trust, Oil Search and AWE Limited – who made the Waitsia discovery in the Perth Basin.

In terms of skin the game, UIL’s directors sit at around 26% ownership – which means that around a quarter of the money so far invested in this company’s future was done so by a group of knowledgeable, experienced players in the world of natural resource production.

Oh, and these seasoned oil and gas stalwarts running UIL threw some $150k in the latest capital raising, indicating they are putting their money where their mouth is, and think UIL has a strong chance of growing in stature over the coming months and years.

What does the future hold for holders of UIL?

Of course, nobody knows exactly what will happen with a speculative micro cap stock like this one.

But what better place to dip into the gas market than WA, an overlooked state who use more gas than any other in Australia ; where natural gas accounts for more than half of the state’s primary energy needs.

Any small player that lands a significant commercial resource could see its share price grow and, consequently, early investors rewarded.

Could UIL follow this pattern? We will have to wait and see...

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.