88E Partner with $1B Premier Oil in North Slope Farmout: Drilling Q1 2020

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

88 Energy (ASX:88E, AIM: 88E) has just attracted a farm-out partner on its multi-billion barrel Project Icewine Conventional play.

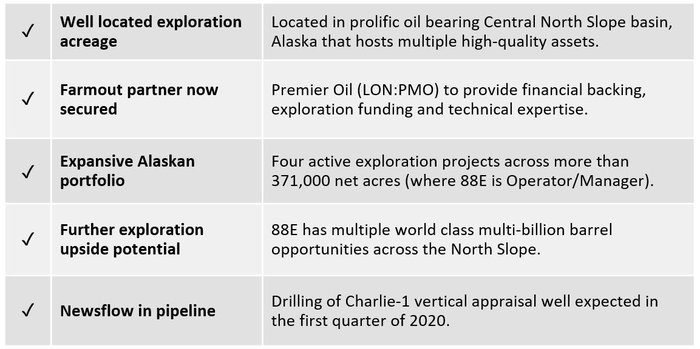

That partner is Premier Oil PLC (LSE: PMO), a £630 million (A$1B) capped mid cap oil company with 80,000 barrels of oil equivalent per day in production.

PMO will be funding an appraisal well up to a total of US$23 million, in exchange for 60% Working Interest (WI) in a circa 40% portion of Project Icewine’s conventional acreage in the area dubbed ‘Area A’ (the Western Play Fairway).

In effect, 60% of 40% = 24% of the conventional Project Icewine acreage has been farmed out.

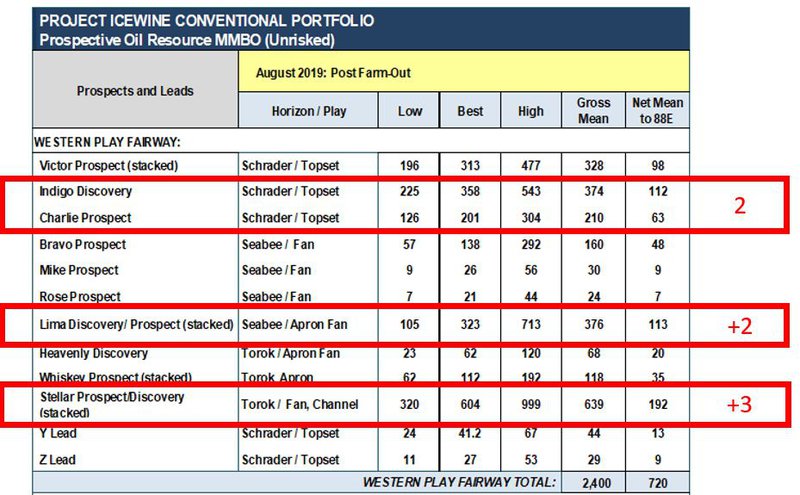

This gives 88E full carry on a US$23M well, which will test seven prospects totalling 1.6 billion barrels – that is 480 million barrels net to 88E at its 30% WI.

88E also retains operatorship and can keep a lid on costs and make sure its objectives are met when it comes to testing the potential here.

It’s important to note that the farm-out does not include the unconventional HRZ shale play – that 0.8-2 billion barrel prospective resource is still with 88E. The HRZ will also be logged and sidewall cores taken in the full carry well with PMO – so that is a bit of a bonus to 88E as well.

The question 88E investors are currently trying to answer for themselves is – what percentage of the company’s assets has it just effectively sold, and how does it compare to 88E’s current market cap?

The answer to this is not an exact science.

But to start thinking about arriving at an answer, it worth considering what percentage of 88E’s market cap would the HRZ shale play be worth?

Let’s apply some rough numbers.

Say you attribute 50% of 88E’s current circa A$100 million (US$68M) market cap to the HRZ shale play.

On that percentage basis, PMO have bought effectively 24% of 50% of 88E’s assets – which is 12%. And PMO is paying US$23M for that right.

On that basis, an implied valuation for Project Icewine (alone) would be US$192 million (A$283M) — with 88E's share almost double the company’s current market capitalisation.

Now, unpacking the deal further still, the other element to consider is the option for PMO to earn up to 50% WI in Area’s B and C of 88E’s conventional acreage at Project Icewine — if the appraisal well next quarter in Area A is successful.

PMO could do that by spending a further US$15M.

On success, the equation changes completely – for 50% of 35% of the Project Icewine conventional acreage, it would probably be worth less than 10% of 88E’s value at that point – as the successful well would have re-rated the company and its Western Margin acreage.

So on success, and those rough estimates, that would be US$15M for circa 1.75% of 88E, and an implied 88E valuation of US$860M – 8 times greater that 88E’s current market cap.

I want to stress that these numbers are extremely fuzzy – arriving at valuations of companies is more art than science sometimes, especially at the speculative end of the market.

But however you look at it, it does look like a great deal for 88E at this point in time.

And, we haven’t even mentioned 88E’s Yukon or Western Blocks assets in all of this.

We have been following 88E for years now, and whilst there have been ups and downs like any speculative oil explorer, it looks like the coming months are going have significant news (and hopefully oil) flowing.

Share Price: $0.016

Market Capitalisation: $101.3M

Here’s why I like 88E:

88 Energy’s (ASX:88E, AIM:88E) strategy to pursue high reward oil projects on the prolific North Slope of Alaska hasn’t gone unnoticed as evidenced by today’s farmout for its conventional prospect portfolio at Project Icewine.

88E is the kind of stock that is not for the feint of heart – the company moves very fast and continuously takes well-calculated risks that allows it exposure to outsized returns. Such is the binary outcome nature of speculative oil investing, rewards from success in this game can outweigh risks by orders of magnitude.

88E’s new partner PMO has made some big discoveries in the past, back in 2015 on the Falklands Islands, hitting a total hydrocarbon net pay of 136 feet, and more recently Zama – offshore Mexico, where initial gross original oil in place estimates were in excess of 1 billion barrels.

So PMO is the kind of company with the technical chops to complement 88E’s high calibre exploration team and accelerate the chances of a large discovery in the near term.

Given PMO’s relatively nimble size, we would expect them to move a lot faster than a major oil company would, where sometimes there can be a risk that projects get shelved for years.

PMO and 88E will certainly not be moving slowly, and are aiming to drill the appraisal well in Q1 2020.

As we mentioned earlier, that well is going to test 7 stacked conventional targets – including all the primary targets 88E has identified – equating to circa 480 million barrels net to 88E post farm-out.

Even after the reduction in WI, this a sizeable target for any oil company, let alone a junior like 88E.

Plus given that 7 targets will be tested with one well alone, it means 88E has avoided having to do a multi-well farm-out deal with a major, which would have been a costly and dilutive exercise.

PMO was obviously impressed with the work 88E has done to date, going so far as to call 88E’s Torok targets ‘discoveries’ – which is a huge validation of 88E’s progress.

Plus overnight in London in its investor presentation, PMO was already referring to “first production” timelines before the well is even drilled – so there is clearly a high level of confidence that they are onto something.

PMO traded up 10% on their results overnight in London, so they must be doing something right.

If one thing is for sure, 88E are always on the look out for the next big opportunity with a focus on the North Slope of Alaska, and the company is now pursuing multiple high potential projects across 4 projects.

88E itself is the operator on four active exploration projects across more than 500,000 acres.

Alaska North Slope Basin

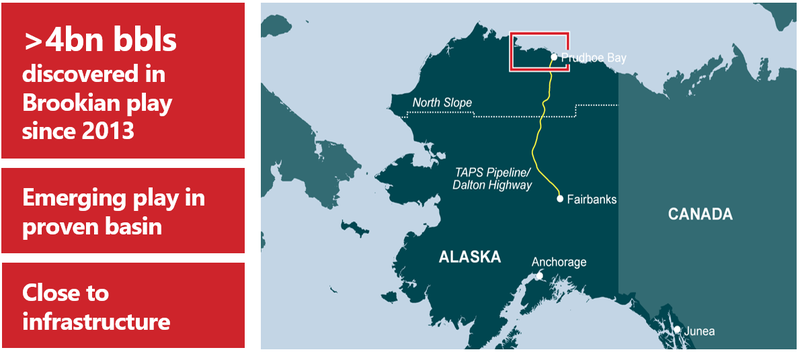

Alaska’s North Slope basin is super prolific when it comes to oil discoveries and has seen renewed industry interest of late.

Over the last six years, more than four billion barrels of oil have been discovered in the Brookian play, which is a staggering amount for one small corner of the world.

While the historical focus was mainly on the deeper Jurassic/Triassic Ellesmerian Play, the under-explored conventional Cretaceous Brookian play has been unlocked in recent years through technological advances and associated discoveries.

The considerable recent industry interest at the North Alaska Slope has been driven by these technological advancements, enabling these once stranded resources to be commercialised.

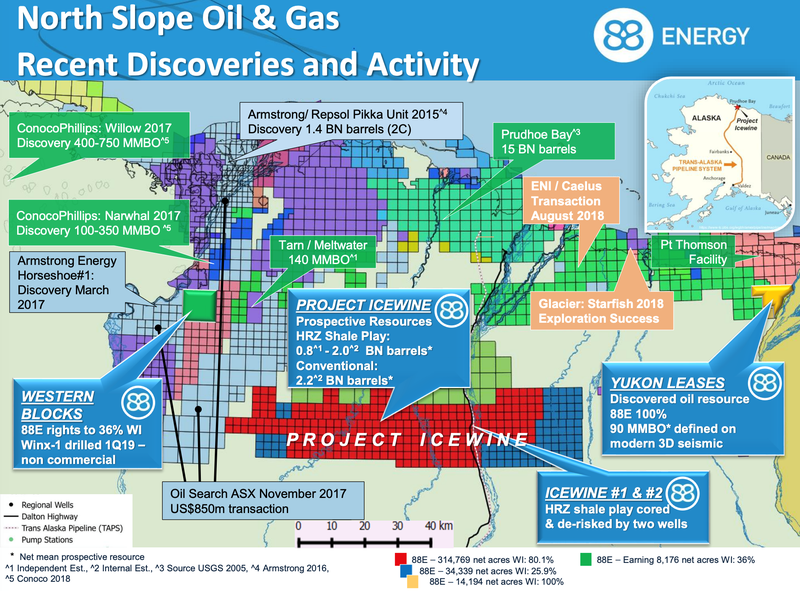

Several developments, not unlike that of 88E’s, are already underway at various levels of maturity involving operators such as ConocoPhillips, ENI, Repsol and Oil Search.

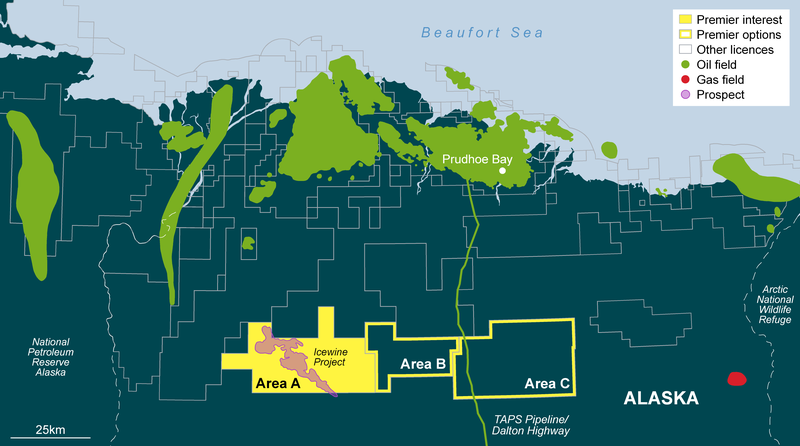

The following map is a snapshot of the hive of activity that surrounds the Project Icewine territory, highlighting the presence of big players such as Conoco Phillips, Armstrong Energy and Australia’s Oil Search (ASX:OSH).

While interest in the region is ongoing, it has already led to a number of major transactions including Oil Search’s (ASX:OSH) $850 million entry to the North Slope, ENI’s (NYSE:E) purchase of Caelus Energy exploration acreage and ConocoPhillips’ (NYSE:COP) asset swap with BP (LON:BP) combined with exploration success and development.

Located in the proven Alaska North Slope basin, close to the Trans-Alaska Pipeline and the Dalton Highway, 88E’s Project Icewine consists of 528,099 contiguous acres with access to these transportation corridors.

Project Icewine Conventional Farmout Executed

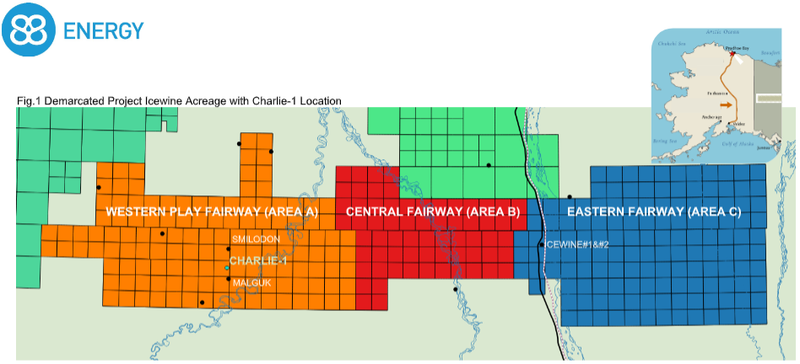

The news overnight of 88E’s farm-out process for its conventional prospect portfolio at Project Icewine, involved the £581.90 million (A$1.04B) capped Premier Oil PLC (LON:PMO) signing a Sales and Purchase Agreement with 88E and its JV partner, Burgundy Xploration LLC, to farm into Area A of the JV’s Project Icewine acreage.

Under the terms of the agreement, Premier will pay the full costs of an appraisal well which will be up to a total of $23 million, to test the reservoir deliverability of the Malguk-1 discovery.

On successful completion of the work programme Premier will earn a 60% paying interest in Area A, while 88E will retain a 30% working interest in Area A.

Note that this is just 60% of approximately 40% of the acreage, as the farmout only covers one area — Area A initially.

On completion of appraisal, it will also have the option to acquire 50% of Area B or C (an additional 40%) for spending $15m if the Charlie-1 well in Area A is successful, which could include a well

88E will retain control of the drilling for now, continuing to operate the Charlie-1 well via its wholly owned Alaskan subsidiary, Accumulate Energy Alaska Inc.

The agreement will provide financial backing, exploration funding and technical expertise for the project, while allowing 88E to maintain a material interest in the project.

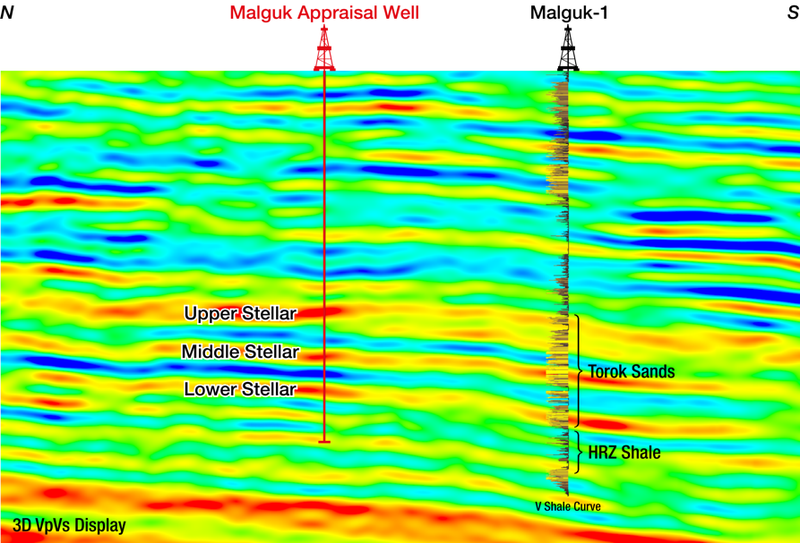

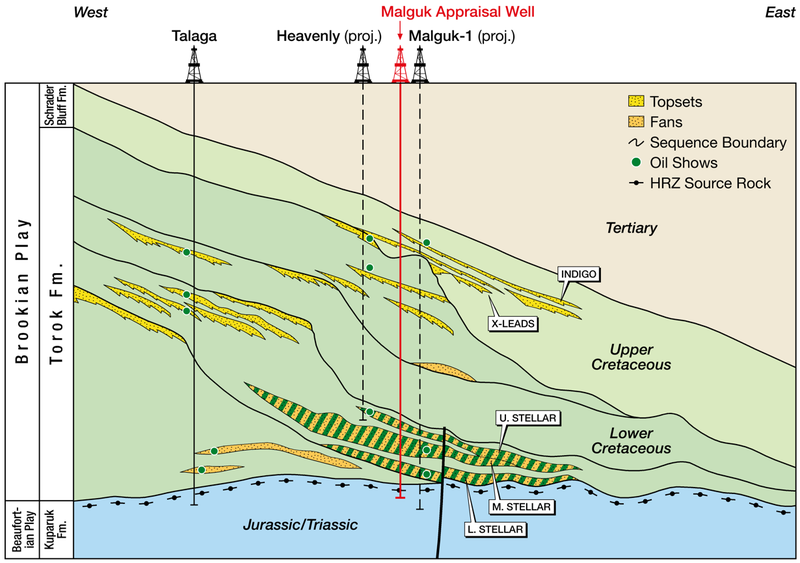

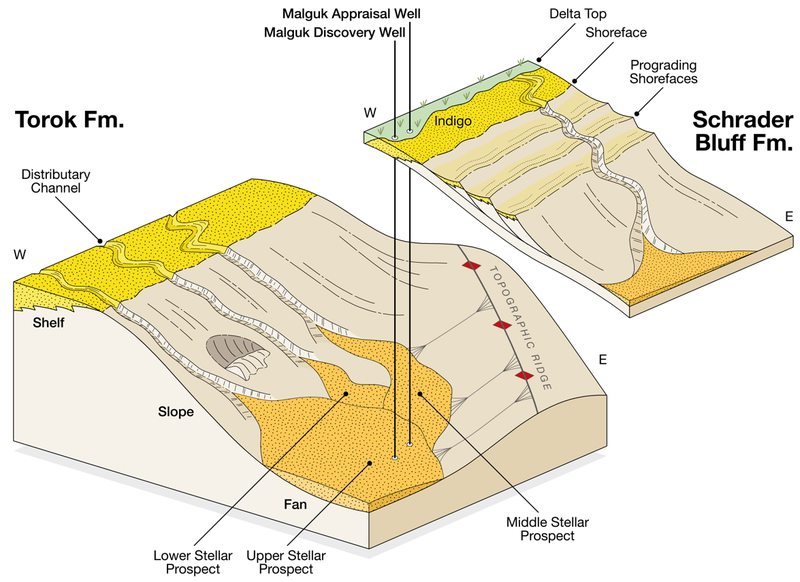

Area A (shaded in yellow above) is in the western section of Project Icewine, and it contains the Malguk-1 discovery, which was drilled by BP in 1991. The discovery well encountered 251 feet of light oil pay in turbidite sands in the Torok formation, within the recently emerging Brookian play.

Here you can see Area A, or the Western Play (in orange), the Malguk-1 discovery, and the Charlie-1 appraisal well, alongside Central Fairway (Area B) and Eastern Fairway (Area C):

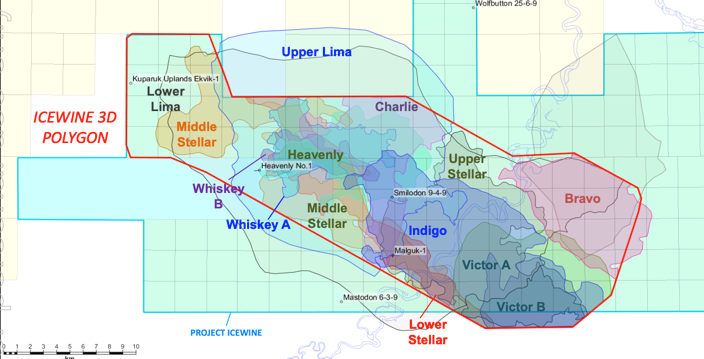

The Charlie-1 appraisal well — which will be operated by 88E — has been designed to test all of the prospective horizons identified in the Western Play Fairway, giving benefits usually only derived from an expensive multi-well program.

The Charlie-1 well location conveniently intersects seven stacked targets, including all the primary targets – 1.6bbl gross, of which 480mmbbl net to 88E on the reduced Working Interest.

And given that 88E is operating the well, it is able to retain control in house of the drilling process and costs, of which it is already well progressed with rig contracts expected to be signed in the near term.

Based on the original well data and its evaluation of the existing 3D dataset, Premier estimates an accumulation of more than 1 billion barrels of oil in place – just in the Torok.

Drilled by BP in 1991, the Malguk-1 discovery well hit 251 feet of light oil pay in the Torok formation.

88E and PMO’s upcoming appraisal well will test the reservoir deliverability of the Torok Formation, and also additional prospectivity in the Schrader Bluff Formation.

Schrader Bluff formation

88E last year updated the conventional prospective resource at Project Icewine based on the newly processed 3D inversion dataset.

This data highlighted features, such as feeder channels, associated with the prospects, providing further confidence in the mapping and the geological model.

Additionally, further analysis provided positive insights into the prospects / discoveries identified in the shallow Schrader Bluffs Formation, as well as the deeper Torok Formation – which appears to be what piqued PMO’s interest in the project.

PMO sees there also being considerable upside in the shallower Schrader Bluff formation which has yet to be explored, in a play similar to the Pikka/Horseshoe trend, which lies to the north-east of Project Icewine.

88E has also indicated that it thinks one of the Schrader Bluff targets could well be a discovery.

More on Premier Oil PLC (LON: PMO)

Premier Oil is a company that ASX investors may not be familiar with, however it is well known in the smaller end of the market in the UK.

PMO has a strong track record of delivering projects through to production in challenging environments, with an experienced management team with deep industry knowledge. Most recent reserves reported were around 867 mmboe (as at 31 December 2018).

The company’s portfolio of production projects is spread across three global regions, having made some big discoveries in the past.

These include in the Falkland Islands where in July 2012, Premier farmed in for 60% of Rockhopper's Exploration licence interests in the North Falklands Basin, including the Sea Lion discovery.

More recently Premier raised it resource estimate at the Zama oil field in the shallow water Sureste Basin in the Gulf of Mexico.

From a technical perspective Premier is an excellent partner for 88E. We also like that it is not a $10BN oil behemoth like say BP or Conoco— as unlike partnering one of the big boys, Premier isn’t likely to delay exploration or bully its partners.

So for 88E, this deal strikes a good balance between cultural fit and value.

Plus, the way the deal has been structured results in a meaningful working interest being retained by 88E for its shareholders.

Given Premier’s technical calibre, the partnership is a solid strategic move by 88E that adds to the JV.

For Premier, this is a cost effective entry point into an emerging play – following recent advances in drilling and completion techniques – in a proven oil province which has the potential to deliver significant organic growth opportunities for the group.

Sounds like a win-win outcome to us. All that is left is to finalise the paperwork, and plan the Q1 2020 drilling event.

Project Icewine Unconventional Update

The farm-out with Premier Oil at the Project Icewine does not involve the unconventional HRZ prospect and 88E retain 100% of the rights to that play.

The finalisation of advanced analysis using state-of-the-art technology has significantly improved the 88E’s understanding of the nature of the HRZ play and identified the HRZ as an excellent source rock with good potential as an economic shale play.

Next Steps

With plenty of upcoming newsflow in the pipeline, 88E is worth keeping a close eye on.

Shareholders should benefit from accelerated newsflow given that the Project Icewine conventional farm-out is now sorted and the JV partners will be drilling a vertical appraisal well in the first quarter of 2020.

Rig options have already been identified and contracting negotiations are underway ahead of the well being drilled and tested in Q1 2020.

Permitting is on track with amendments to key permits for the drilling of the Charlie-1 well having been submitted, while standard completion documents have been agreed and are in the process of execution, including the Joint Operating Agreement and assignment forms.

The group also expects to be in a position to drill a lateral side track appraisal well in the fourth first quarter of 2020, with development drilling pencilled in for 2024 prior to first oil in 2024-25.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.