Why has this stock got analysts predicting four thousand percent gains?

Published 26-AUG-2013 12:28 P.M.

|

21 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

At The Next Oil Rush, we’ve been seriously enthusiastic about the incredible opportunities emerging in Africa lately, and as you know we’ve got a stellar track record of picking the best African oil explorers – and this junior oil explorer is no exception.

As you’re probably already aware, Angola, Nigeria, Algeria, Libya, Gabon and Egypt have all proven to be the continent’s oil and gas powerhouses to date...

... But we wanted to let you in on this latest news about Morocco’s previously untapped oil and gas potential as the next big investment opportunity that we are jumping on right now.

10 wells are about to be drilled offshore Morocco in 2014 alone – making it the fastest pace of drilling seen in the region since at least 2000.

Morocco has been proclaimed the new Angola when it comes to potential top oil-producing African nations. In fact, Morocco is one of the most under-explored nations for oil so far – but that’s about to change, and the junior oil company we are writing about today is positioned front and centre to ride the wave.

This junior oil company is capped at around AUD $60 million, but have just had their share of a Moroccan offshore oil asset valued at US $1.8 billion by a major US oil player who is who recently gobbled up our junior explorer’s much larger JV partner (more on this stunning valuation later in the article)

We believe that this valuation will only increase once they drill this prospect in the coming months, and even sooner as directly neighbouring blocks are drilled by Total, Chevron and Genel (10 nearby wells coming up in 2014 alone!)

We’ve been following events in Morocco as they unfold. One junior oil company has been repeatedly coming onto our radar for all the right reasons – and we’ll show you why it’s literally got professional industry analysts jumping up and down in excitement and throwing around predictions of four thousand percent gains.

This company has also acquired an impressive oil block offshore in Gabon (where a nearby discovery has been made just a few days ago), has recently successfully secured $12 million in funding in a very tough market AND has significantly come off recent stock price highs, presenting a buying opportunity that the team at The Next Oil Rush has been taking advantage of.

We are pleased to introduce Pura Vida Energy (ASX:PVD) – You heard it here first:

PVD was an early mover into the potentially rich offshore Moroccan fields, having secured the highly prospective Mazagan block offshore Morocco.

PVD then announced what has been touted by industry as one the most lucrative farm out deals EVER signed in the region.

Here’s the deal: US listed $19 billion Plains E&P (NYSE:PXP) had agreed to fund the ENTIRE COSTS for drilling not one, but TWO offshore exploration wells in the Mazagan field in return for 52% of the block.

PVD kept 23% of the highly prospective block and do not have to pay a single cent for the first two wells... AND they also get a US $15 million sign on bonus on final government approval of the deal, expected in the coming weeks.

Now THAT is an excellent deal for PVD, and The Australian newspaper certainly agrees:

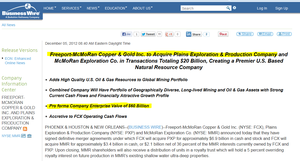

News just in – PVD’s generous farm in partner Plains E&P was recently taken over by an even BIGGER oil and mining giant called Freeport-McMoRan (NYSE:FCX), who have valued PVD’s offshore Morocco field at US $4.1 billion, valuing PVD’s 23% share of this field at US $1.8 billion... Not bad for a $60 million company, eh?

As if Plains E&P’s pockets weren’t already deep enough as a farm in partner for PVD, the US $60 billion Freeport McMoRan pockets are even deeper .

Stay tuned for more details on Freeport’s important US $4.1 Billion valuation of its 52% interest in the Mazagan field later in this article – this stunning information was uncovered by The Next Oil Rush team, buried in the depths of publicly available merger and acquisition documents from the Freeport takeover of Plains E&P and we will share it with you today.

Investors who bought in to PVD early at 20c per share last year are thrilled at PVD’s success over the last 12 months. As professional stock analysts proclaimed PVD the best performing IPO for 2012 , shareholders saw the stock price rise 400%.

But, due to the recent overall negative market, PVD’s stock price is currently down to much lower levels – which is great news for the team at The Next Oil Rush – we have been taking the opportunity to add PVD to our portfolios as a long term play.

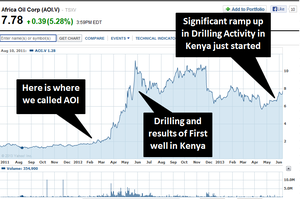

Regular readers of The Next Oil Rush will be familiar with our long-standing interest in oil exploration in Africa – specifically in AOI, which was our ‘ tip of the decade’ in February 2012 at around CAD$1.8 and has been as high as CAD$11.25 since, currently trading at around CAD$8

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance

Given our success with calling AOI, we are very excited to have discovered West African explorer PVD

However, given what we’ve uncovered about the company we believe these current price levels won’t last long.

Keep reading to find out why...

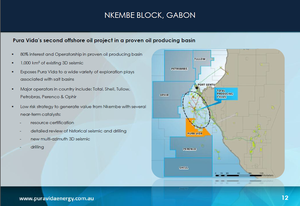

PVD acquires offshore block in Gabon

PVD has just announced its acquisition of the Nkembe block offshore Gabon. With this potentially rich field in hand, we can expect more great things from PVD in 2013.

PVD is currently on the look out for farm-out partners, with their data room for their newly acquired Gabon Block opening in August for interested JV partners.

The new Gabon block is located right next door to blocks that are already producing oil, and owned by some of big names in the Oil & Gas game like Total, Shell, Tullow, Petrobras, Perenco and Ophir

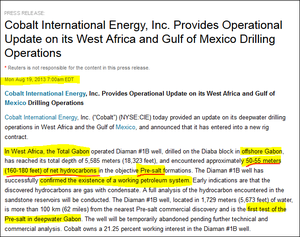

NEWS JUST RELEASED by a company drilling near PVDs Gabon Block:

This breaking news is very significant for PVD as it is the first EVER pre-salt discovery in Gabon. (PVD is drilling pre-salt targets nearby). This announcement is saying that they have confirmed a working petroleum system in the pre-salt (it means there is oil!) and hence has significantly de-risked PVDs Gabon assets.

This couldn’t be timelier for PVD given that they are currently working to bring in a partner on the Gabon block....

...Looks like the power at the negotiating table has just swung very heavily in PVD’s direction.

Professional Stock Analysts agree – PVD is expected to do some very big things

It’s always a good sign when professional analysts are as excited about a company as we are (click on any image to view the full report):

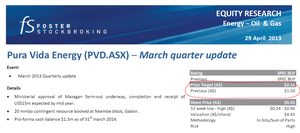

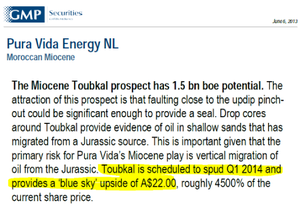

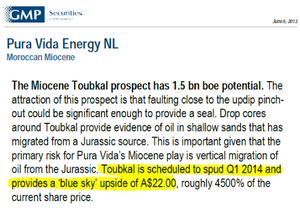

The analyst at GMP Securities provides a ‘blue sky’ upside of AUD $22.00 , roughly a 4500% increase on the current PVD share price :

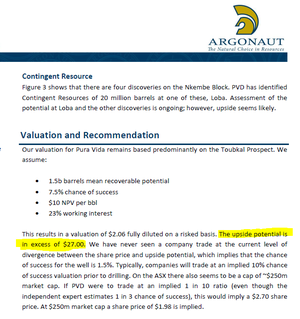

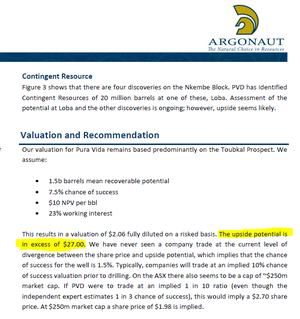

A highly respected analyst from Argonaut calculates PVD shares could have blue sky potential of up to $27.40 on successful drilling:

In this article we explore:

- About PVD

- Why Morocco is shaping up to be THE next big story in oil exploration

- Asset 1: PVD’s Moroccan Mazagan offshore oil block – worth $1.8 billion to PVD?

- Asset 2: PVD’s Gabon field – what’s the skinny?

- Why we have invested in PVD – in a nutshell

- An analysis of PVD against some of our 20 Pre-Investment Check List Criteria.

About PVD

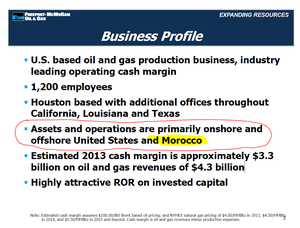

Pura Vida Energy is an ASX-Listed oil explorer building a portfolio of high quality assets in Africa. PVD currently has operations offshore Morocco and Gabon with significant resource potential.

If you haven’t heard of PVD yet, here’s the lowdown – this article was published in the West Australian newspaper about 6 months ago:

...and the great news for us is that PVD stock price has come down since this was published, giving us a great chance to take our position.

So why all the fuss about Morocco?

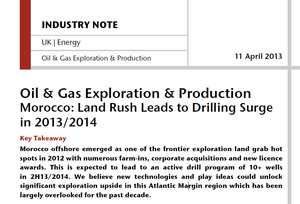

Morocco offshore emerged as one of the frontier exploration land grab hot spots in 2012 with numerous farm-ins, corporate acquisitions and new licence awards.

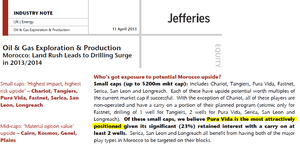

An industry research note released by London based global investment bank Jeffries in April presents an excellent and highly detailed analysis of why offshore Morocco will be the next hot region in oil exploration:

You can download the Jeffries Report here. ( http://www.puravidaenergy.com.au/news_pdf/Jefferies_Morocco_Note_April2013.pdf )

In their overall analysis of oil & Gas in Morocco, here is what they had to say about PVD:

This video shows Zac Phillips. Oil & Gas Analyst at Fox-Davies Capital talking about the opportunities and amazing potential in offshore Morocco– PVD gets a mention:

Interesting to note is the efforts by the Moroccan government to revise their oil exploration, investment and taxation laws to attract foreign companies to the country. PVD has certainly taken advantage of this.

The following video shows a news report about the favourable changes for oil explorers operating in Morocco:

And yet another mention of PVD:

As mentioned by the reporter...we certainly agree that 7 billion barrels of oil is a “very large amount”!

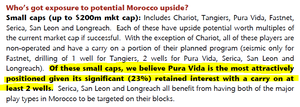

A wide range of mid and large cap companies flocked to Morocco last year, planning an active drill campaign of 10 or more wells in the second half of 2013 and 2014.

PVD was an early mover in offshore Morocco... Any nearby oil strike there will directly impact them.

Other small caps with acreage in offshore Morocco include Chariot, Tangiers, Fastnet, Serica, San Leon and Longreach. However, analysts have zoned in on PVD as THE most attractive .

In fact, at The Next Oil Rush , we can confidently say we’ve never seen such a wide gap between a company’s potential and its current market capitalisation.

PVD Asset 1 – 23% of the The Mazagan Field in Morocco... and it’s worth US $1.8 billion

Why is PVD’s Moroccan venture so promising? Offshore Morocco has a lot of geological similarities to the already successful oil discoveries in the US Gulf of Mexico

PVD’s technical team has extensive experience in the Gulf of Mexico, which is likely why they are now pursuing opportunities in Morocco and Gabon.

Analysts predict PVD’s first Mazagan drill in Q1 2014 could add over $20 per share

Just in case you weren’t amazed enough the first time around – here are those analyst price predictions again...

The Toubkal prospect is the first to be drilled in PVD’s Mazagan field and is an analogue of the billion barrel Jubilee field in Ghana – the largest oil discovery made in West Africa in the past decade.

The Toubkal Prospect is scheduled to be drilled in Q1 2014 and it certainly has analysts excited – with valuations of over $20 per share for PVD being thrown around.

One analyst at GMP Securities provides a ‘blue sky’ upside of AUD $22.00 , roughly a 4500% increase on the current PVD share price :

A highly respected analyst from Argonaut calculates PVD shares could have blue sky potential of up to $27.40 on successful drilling of the Toubkal prospect:

We are taking this opportunity while PVD stock is trading relatively low and before the market twigs to this incredible opportunity.

This video was filmed over a year ago, and shows PVD CEO, Damon Neaves explaining why PVD is so excited about their Morocco acreage and value proposition

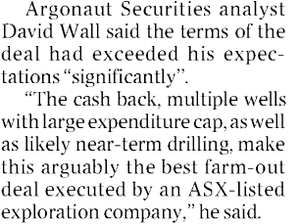

PVD Morocco: Farm-out Deal of the Decade?

We have already talked about the farm-out that PVD secured on their Moroccan Mazagan block to get free carried on $215 million worth of offshore drilling AND a US $15 million upfront payment on government sign off.

Basically what this means is that in return for 52% of the block, Plains E&P agreed to fund the two offshore wells and do all the work, and PVD just sits back and watches, waiting for the $20 plus per share kick in the share price predicted by analysts on a successful well.

Here is a snippet from an article in The Australian newspaper:

And from the GMP Securities research note on PVD:

So if that wasn’t already an excellent deal – along came global resources giant Freeport...

Freeport-McMoRan acquire Plains E&P, Values Mazagan field at $4.1 Billion dollars

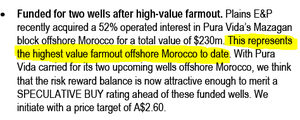

In May 2013, PVD’s partner on the Moroccan Mazagan field, Plains E&P was gobbled up by $60 billion resource giant Freeport-McMoRan (NYSE:FCX). The Next Oil Rush discovered that Freeport-McMoRan values their 52% interest in the Morocco Mazagan field at US $4.1 billion , hence PVD’s 23% share at US $1.8 billion – incredible news for current and prospective investors alike.

The following video shows some analysis on the Freeport-McMoRan acquisition of Plains E&P

http://youtu.be/MZxDdyRJc5Q?t=12s

Some more analysis on the deal:

Freeport has stated that their only INTERNATIONAL offshore oil license is in Morocco (the same one they acquired form the Plains E&P takeover... the same one on which they are “free carrying” PVD).

You can see here from the Freeport presentation that was made to investors in New York:

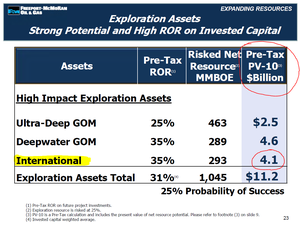

According to Freeport McRoRan its 52% interest in the Mazagan field in Morocco is worth $US 4.1 billion! This makes PVD’s 23% share worth $US 1.8 Billion!

This is staggering for a $60 million dollar company like PVD – just remember you heard about them first here at The Next Oil Rush.

PVD Asset 2: Newly acquired Gabon field – Can PVD repeat its Moroccan farm-out success?

Also in February this year, PVD announced its acquisition of the Nkembe block in Gabon – potentially their next Mazagan:

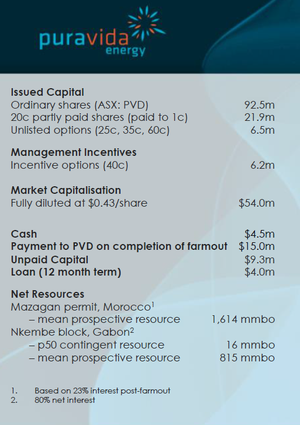

Investor presentation from PVD April 2013:

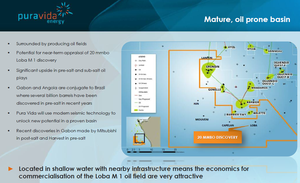

The more mature, prolific shallow water basin peppered with proven fields and a number of nearby discoveries by some of the biggest companies in the world looks very good indeed. Total Energy has 100,000 barrels of oil pumping out every day from nearby wells, which bodes well for this new acquisition.

High impact wells are being drilled near PVD’s new field as we write , and results are expected to be coming in thick and fast over the next 12 months – which will have carry on effects for the value of PVDs block (as mentioned earlier, a significant result has just been announced nearby)

The great thing about PVD’s new Gabon field is that operational costs are lower than the Mazagan field, with the shallower waters (50-500m deep compared to 2 km in Morocco) and closer proximity to infrastructure.

PVD has an 80% equity position with the Gabon government holding the rest. The block is conjugate geologically to Brazil, where several billion barrels have been discovered in recent years.

Shell operates the giant Rabi-Kounga oil field onshore Gabon with reserves of over 800 million barrels. Recent discoveries in the area by Harvest (NYSE:HNR) and Mitsubishi suggest great oil reservoirs in the area. PVD has existing wells along the block where oil has been discovered.

Here’s PVD’s Managing Director, Damon Neaves, speaking about the new Gabon prospect:

The block is also close to already producing fields and existing infrastructure, with major operators including Total, Shell, Tullow, Petrobras, Perenco and Ophir.

The next step for PVD is to establish a farm-out deal on the 1210sqkm Gabon block, in a replication of their already successful Moroccan strategy.

We expect to see a similar value creation path as the Mazagan permit in Morocco as PVD progresses its work program over the next 12 months. The company has outlined a low risk strategy to generate value from Nkembe with several near-term catalysts:

- Resource certification

- Detailed review of historical seismic and drilling

- Farmout

- New multi-azimuth 3D seismic

- Drilling

PVD plans to open the data room in August to start the farm-out process of its Nkembe block, and the recent discovery nearby should certainly stoke significant interest and place PVD in an excellent position at the negotiation table.

All the key ingredients are in place for significant value to be added over the next 12 months as the asset is de-risked through the acquisition and processing of 3D seismic, delineation of resources, prospects and leads at the pre salt layer a farm-out being concluded and ultimately the drilling of a well.

Why Have We Invested? In a nutshell...

PVD has achieved all its stated milestones for 2012 and we expect this strong delivery will continue in 2013 and 2014. PVD’s early entry strategy has generated significant revenue.

PVD stated activity for 2013 included:

- Significant nearby drilling activity in both Gabon and Morocco leading into Mazagan wells

- Value-creating work program on Nkembe block in offshore Gabon

- Farmout of Gabon to secure finding for forward work program, including drilling

- Continuation of growth strategy through new ventures

Analysis of PVD using our pre-investment checklist

The Next Oil Rush Pre-Investment Checklist Criteria was created by a team of contributors that has been successfully investing and trading speculative stocks for many years.

The check list outlines key aspects to research and understand prior to making an investment in a speculative stock.

We have analysed PVD against a few of the pre-investment check list items here:

- Business Plan: What is the company’s business plan?

One of PVD’s core objectives is to build a diversified portfolio of oil and gas assets over time. The acquisition of the Nkembe block in Gabon is an important step in the execution of that strategy which balances the portfolio by adding near-term, low risk appraisal drilling plus exploration upside.

The Company is continuously reviewing opportunities throughout the African region which are complementary to its existing assets and consistent with growth and capital management strategy.

2. Cash: Does the company have cash in the bank? What is the rate of cash burn? Does the company have debt?

PVD recently raised $12m ($8m equity and $4m debt) and reduced its debt position from $6m to $4m.

PVD is also expecting a US $15 million sign on payment when their Moroccan farm-out is approved.

This will be more like AUD $16.5 million of the AUD keeps plunging against the greenback!

PVD also recently announced that core inspections it performed on previously drilled samples from their new Gabon block has confirmed the presence of a significant oil column – PVD now plan to appraise and potentially develop this smaller field for near term production and cash flow .

This is a solid cash flow strategy we feel very comfortable with.

3. Management: What is the track record of management? Does management own stock in the company?

PVD’s management team is, quite frankly, impressive. It includes extensive commercial technical and A & D expertise with a track record of exploration success and value accretive acquisitions.

And yes... the management own stock in the company... in fact they own a lot of stock!

According to the GMP securities note, Board and Management own a whopping 34% of PVD. You can bet they will be taking their jobs very seriously as it is their money on the line too!

4. Backers: Are there any high profile investors or backers?

PVD’s farm-out to PXP earlier this year was completed at the most attractive terms to date.

The US $230 million farm-out of the Mazagan permit means PVD is now fully funded in its deep water drilling campaign offshore Morocco, which begins in Q1 next year with the Toubkal-1 well targeting 1.5 billion barrels (mean).

While other small players were able to achieve a one-well carry with a cap, PVD will be carried free for two wells, allowing the company to drill the 1.5 billion barrel Toubkal prospect, and test a second play type should this well be unsuccessful.

The PXP farm-out also means PVD can diversify its resource portfolio with low risk, near-term appraisal drilling to commercialise the 20 million barrel Loba Oil Field in the Nkembe block scheduled to start in 2014.

PLUS FCX’s recent takeover of PXP means PVD now has an EVEN BIGGER backer – one that has valued PVD’s 23% of the Mazagan licence at US $1.8 billion.

5. Price Catalysts: Are there upcoming catalysts?

PVD is extremely undervalued at the moment, but, over the next few months, The Next Oil Rush team expects a number of significant catalysts to move share price, including:

- Contracting of a rig to drill offshore Morocco

- Receipt of $15 million on Moroccan government sign off – expected any week now

- Other drilling nearby from August

- Gabon farm-out

- Market wake up to FCX’s $1.8 billion valuation of PVD’s 23% of the Morocco field.

Extensive regional drilling programs are about to commence in Morocco and Gabon. The second half of 2013 will see a renaissance period emerging in the Moroccan oil industry with the first of up to 10 offshore wells drilled.

We expect over the coming months to get further visibility of the schedule for the drill ship being used. Any success by operators adjacent to PVD will serve as a major catalyst for the company.

Five wells with multibillion barrel potential are also scheduled for Gabon in late 2013 and, again, any success by regional operators will have positive implications for PVD.

Our Conclusion

PVD’s track record over the last 12 months has been remarkable, with a 400% ROI for early investors contributing to analysts proclaiming the company the best performing IPO in 2012.

But because PVD’s share price has been taking a beating lately, we’ve been taking the opportunity to buy ahead of what The Next Oil Rush team predicts will be a market recognition of this junior oil company’s incredible prospects.

The core of PVD’s success is its early move on the highly prospective Magazan block offshore Morocco, Africa’s next big frontier for oil.

The Mazagan block’s main attraction for investors is strengthened by the number of other small, medium and large caps engaging in high impact drilling in the area – and of these, analysts agree PVD presents the stand out opportunity by far.

PVD’s potential was undoubtedly also bolstered by PXP’s US$215 million farm-in for a 52% share + $15 million up-front payment on the soon-to-be-complete government sign off.

Now FCX’s takeover of PXP and its subsequent valuation of PVD’s Morocco field license at US $1.8 billion can only increase market interest in the company.

PVD has also proved its smarts by raising a further $12 million capital in a very tough market.

In addition, a significant number of catalysts over the next 12-24 months are combining to make 2013 a landmark year for the company, so we expect our investment in PVD to continue to rise..

These include:

- Contracting of a rig to drill offshore Morocco

- Receipt of $15 million from PXP on government sign off – expected any day now

- Other drilling nearby from August

- Gabon farm-out

- Market wake up to FCX’S $1.8 billion evaluation of the Morocco field.

Most exciting is PVD’s continued diversification of its resources portfolio into the proven mature oil fields at Gabon, with the recent acquisition of the Nkembe block.

The company’s experienced management team has clearly identified both blocks as featuring geological similarities to the already productive Brazilian acreage, and has the technical expertise to exploit the full potential of this opportunity.

At The Next Oil Rush , we fully expect PVD to repeat its stunning Morocco farm-out record in Nkembe when it opens its data room in August – remember, it was the Morocco farm-out that originally raised the stock price up a MASSIVE 400%!

The bottom line?

We’re buying PVD while the share price is still relatively low and before the market cottons on to the company’s extraordinary convergence of recent positive announcements and drilling activity heats up in Morocco and Gabon over the next few months.

For up to date information on Pura Vida Energy follow PVD on Twitter and like PVD on Facebook

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.