Drilling in East Africa – Kenya Drill Target Selected For SWE

Published 10-OCT-2014 11:09 A.M.

|

13 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Swala Energy (ASX:SWE) has just selected a drilling target for their Kenyan Block 12B, to be drilled in 2015. SWE’s JV partner, oil major Tullow, have determined a mean recoverable gross oil volume of 44 mmbbls for this prospect, the Ahero “A” prospect. SWE is also expecting seismic results on their Pangani licence in Tanzania in the coming weeks, with drilling of targets also planned for 2H 2015. In the New Year, further seismic results will be delivered for the Tanzanian Kilosa-Kilombero licence – with one prospect ‘Kito’ (151 million barrels gross prospective unrisked P 50 ) identified already, we are hoping SWE can uncover even more drill targets. Still in Tanzania, SWE has listed on the local stock exchange to a positive response – ‘Swala Tanzania’ is up 400% since listing on the Dar es Salaam Stock Exchange (DES). It seems the local Tanzanian people are very keen to invest in oil exploration in their country. The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance. SWE are also working with potential partners on the bidding for the Tanzanian Eyasi Block. SWE’s listing on the local stock exchange has surely boosted SWE’s bidding status for Eyasi in the eyes of the government. We would imagine the Tanzanian government would be under pressure to award this license at least partly to the Tanzanian people – and this could be done very simply by awarding it to SWE and their partner. Plus in Zambia SWE has just received the formal hydrocarbon rights to its first exploration block. In Kenya, in addition to the just released drill target, Tullow and SWE have continued their exploration efforts, with seismic results due in the coming weeks. CEPSA, who had farmed into Block 12B a few months ago, opted to withdraw citing that they would have preferred more time to review the data before committing to drilling. Unwinding the Farm-in has caused some confusion around the right way for CEPSA to return the 25%, which has been referred to arbitration, and will hopefully be resolved in a few months. A small distraction while Tullow and SWE press ahead towards drilling in Block 12B next year. That’s a lot of results due in the coming months for SWE, and we are hoping for even more high potential drill targets to be added to contention for 2015 drilling.

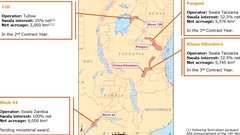

SWE owns acreage in a number of high potential oil spots in and around the East African Rift System, also known as the EARS – arguably one of the most prospective oil exploration regions in the world. 2 – 4 billion barrels of oil have been discovered in the EARS to date. A current snapshot of SWE’s assets is as follows:

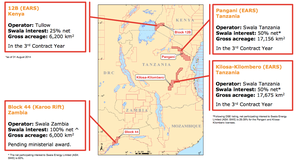

One reason we invested in SWE is the similarities to our Next Oil Rush Tip of the Decade – Africa Oil Corp (TSX:AOI) – after we called it, AOI made region defining oil discoveries in the EARS, with AOI rising as high as 800%:

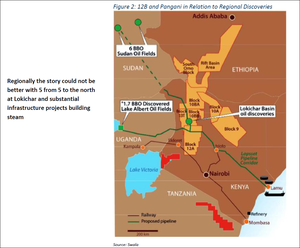

The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance. Africa Oil Corp is continuing to make discoveries within the East African Rift System and we have invested in SWE as they have potential to find more. Both SWE and Africa Oil Corp have the same JV partner, Tullow, and are exploring the very same region. Tullow plan to drill 15 wells in Kenya by the end of 2015 – making for a lot of nearby action for SWE investors. Here are SWE’s blocks (in red) in relation to regional discoveries:

We kicked off our coverage of SWE with The last junior oil explorer operating in this exciting region with this same JV partner went up 800% in a matter of months. This article goes in-depth into SWE’s plans for its EARS oil blocks in Kenya and Tanzania. In SWE up over 50% in the last few weeks, find out why is this only the beginning... we looked at SWE’s plans to expand into Zambia and the knock on effects that AOI’s flurry of EARS oil discoveries is having on SWE’s interests. The momentum kept up with Will This Junior Oil Explorer’s Share Price Keep Doubling? And then in March 2014 SWE hit us with the CEPSA deal – SWE Reveals Mystery US$ 36M JV Partner – Now Circling Multiple Oil Leads... Now as 2015 approaches, SWE is building up for a big year of exploration and drilling and in this article we’re going to bring you up to speed on all the latest plans and ambitions. So what exactly happened with CEPSA?

SWE and Tullow commit to drilling – but CEPSA pull out

Block 12B in Kenya is SWE’s northern most licence in the East African Rift System. SWE, together with JV partner Tullow, have just released their first drilling target on this block – refer below for more details on this target. Previously, SWE had announced a farm in deal with CEPSA. The deal was for CEPSA to pay SWE’s past costs and free carry SWE’s share of up to two exploration wells. CEPSA farmed-in in June, Tullow and SWE committed to drill in July – however it was all moving too fast for CEPSA and they opted to withdraw from the JV. Fair enough. However, unwinding the Farm-in has caused some confusion – the Farm Out Agreement (FOA) says the 25% should go from CEPSA straight back to SWE, which seems the obvious course of action taking the JV back to the original 50/50 split between SWE and Tullow, like CEPSA had never entered the picture. But CEPSA has indicated they will return the 25% to the remaining JV partners under the Joint Operating Agreement (JOA) which states that the 25% be returned to the JV, across all remaining JV partners in proportion to their current holding , which would result in SWE holding 33.3% and Tullow holding 66.6%, not 50/50 as was the original holding – hang on a second... This is certainly an odd situation and a small distraction while Tullow and SWE are pressing ahead towards drilling, but the matter has been referred to arbitration , and hopefully towards a speedy resolution:

CEPSA’s withdrawal came because both SWE and its 50% net interest JV partner and Operator Tullow are pressing ahead with drilling at Block 12B, but CEPSA wanted more time to review the data. During the resolution of the Block 12B withdrawal, SWE have been a little bit quiet. Now that arbitration is underway we expect SWE to get on with exploring a bit more, and to this end they have just released some more exploration news, including a confirmed drill target on the Block:

Drilling next year in Kenya

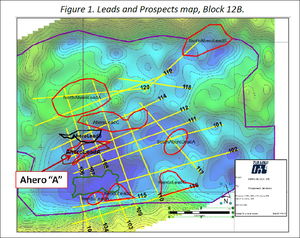

Both SWE and Tullow are committed to drilling Block 12B in Kenya in 2015. At least one target has been identified – SWE has just released details on the Ahero “A” prospect, a mean recoverable gross oil volume of 44 mmbbls. Here is the Ahero “A” prospect on the map below – the dark blue areas are the basin lows (possibly the hydrocarbon source kitchen) and green areas are the structural highs. The seismic lines are in yellow, and you can see the prospect is well covered:

SWE and Tullow have done extensive work on this prospect to date and we are looking forward to the lead up to its drilling next year. It’s all looking very promising at Block 12B for SWE and Tullow. Tullow has just informed Kenya’s government that both companies intend to proceed into the First Additional Exploration Period (years three and four) of the Production Sharing Contract (PSC) they have. In plain English, this means that both SWE and Tullow are obliged to acquire 300 km 2 of seismic data or drill one exploratory well in years three and four of their PSC – and after reviewing all available data, both have chosen to drill a well at Block 12B:

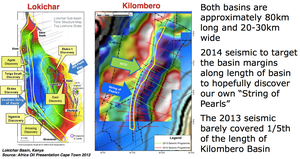

A recently completed seismic survey over Block 12B, plus the news of a firm drilling target, demonstrates that SWE and Tullow have firm confidence to press ahead with work there and commit to drilling an exploratory well in 2015. We should see the results of this seismic surveying soon – hopefully with some more fat drilling targets clearly visible. CEPSA withdrew from the PSC saying it would have preferred more time to review the data before having to commit to a decision to drill or not. But the recent seismic data SWE acquired for Block 12B has given both SWE and Tullow the technical comfort to proceed with an exploration well in 2015. So even though it’s a shame to lose a farm-in partner, it’s great to see both SWE and Tullow sticking to their guns and committing to drilling Block 12B in 2015. Remember, JV partner Tullow has a market cap of over 5BN GBP and it’s backing SWE and its 12B project. As we mentioned earlier, Tullow is also a JV partner with Africa Oil Corp (AOI), which is a first mover in the EARS with a focus on the Lokichar Basin in Kenya – an area that’s analogous to SWE’s Kilombero rift.

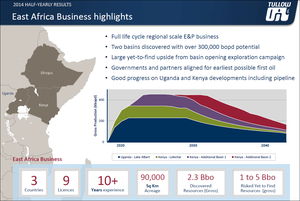

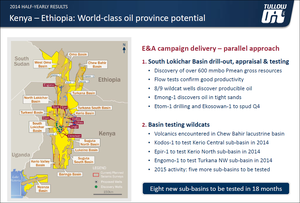

Tullow’s latest half yearly presentation shows just how invested they are in the EARS, after discovering two basins with over 300,000 bopd potential, they are keen to find more oil:

Tullow wont be leaving EARS anytime soon, with eight new sub-basins to be tested in the next 18 months:

Tullow is a 50% JV partner with SWE in Block 12B and the Operator. And now SWE and Tullow are committed to drilling there in 2015. Life definitely goes on after CEPSA – and with a bit of luck and drilling SWE has the potential to follow in Africa Oil Corp’s footsteps and make an oil discovery with Tullow’s help. And it’s not just in Kenya where SWE is accelerating its exploration plans either...

Our Track Record

Regular readers of our sites will be familiar with our long-standing interest in high potential stocks. In addition to TSX:AOI, here are a few more:

- Since the Next Oil Rush article on Real Energy (ASX:RLE), International Feeding Frenzy in Australia’s Hottest Shale Gas Region Puts Undervalued Junior on M&A Radar , RLE has risen as high as 110%.

- After we released the Next Oil Rush article on Rey Resources (ASX:REY), Who is the Mystery Third Man? We Reveal the Next Junior Explorer in WA’s Canning Super-basin... , REY has risen as high as 85%.

The past performance of these products are not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. These products, like all other financial products, are subject to market forces and unpredictable events that may adversely affect future performance.

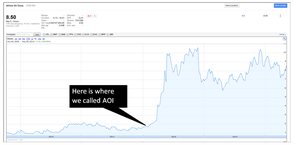

Exploration now official in Zambia

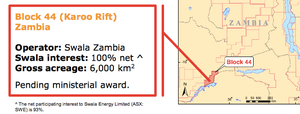

It’s official now – SWE has been formally awarded hydrocarbon exploration rights over Block 44 in Zambia:

Block 44 was offered to SWE back in July and came after over three years of hard work in Zambia to secure an exploration licence. SWE accepted the offer and the Ministry of Energy in Zambia have now formally signed it off.

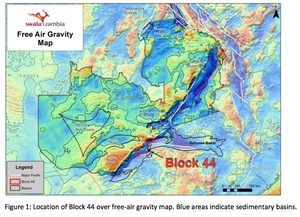

SWE’s exploration projects in and around the East African Rift System now extend from Kenya in the north through to Tanzania in the middle and Zambia in the south. This is a lot of exploration kms in some of the world’s most prospective, yet underexplored oil land. Block 44 covers 6,000 km 2 on the margins of the Karoo aged Kariba Basin, a highly prospective area for gas. The Karoo Supergroup is a stratification layer of rocks around 120M years old that covers two-thirds of Africa’s land mass and holds most of its oil, but it’s thought that the Kariba Basin is likely to be gassy. Block 44 is locked into this system – and the big question is does it any hydrocarbons?

Now that SWE has formal hydrocarbon exploration rights over Block 44 locked in, it will reprocess legacy seismic data drilled by energy giant Mobil in the 1980s and develop its own exploration programme in its first contract year. SWE can withdraw from Block 44 at any time during the first two contract years should the basin’s prospectivity be disproved. We look forward to seeing what SWE can come up with at Block 44 – and once again it’s not the only African country it’s developing oil projects in:

New dimensions for Tanzania

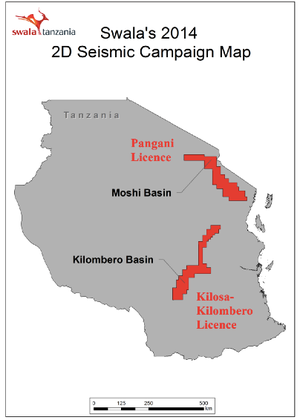

SWE is also attacking oil targets in Tanzania and has two licenses there – Pangani and Kilosa-Kilombero:

SWE is conducting an exploration programme on both blocks to acquire 2D seismic surveys and the first round of results from the Moshi Basin have just come in:

200km of 2D seismic was shot over the Moshi Basin in the Pangani license and preliminary analysis has identified a number of structural leads. SWE says further analysis is expected to define drilling targets for the 2015 exploration programme being planned for its Tanzanian blocks. SWE says now that the survey in the Moshi Basin is finished, the seismic operations will move to the Kilombero basin where a further 430km of 2D data will be acquired in the same area that it identified the Kito Prospect – which independent assessment estimates to hold a gross, best (P50) net resource to SWE of 39.3M barrels:

As long-term investors in SWE this is exactly what we want to see at The Next Oil Rush – step-by-step SWE is going after the huge potential oil resources in and around the East African Rift System and driving exploration toward drilling. It’s not just investors like us in Australia who can now get a slice of the SWE action:

Swala Oil and Gas (Tanzania) Plc has become the first oil and gas exploration company to be accepted and listed onto the Dar es Salaam Stock Exchange (DES) in Tanzania. Official listing of Swala Tanzania on the DES occurred on Monday 11 August. Using this new listing, local investors in Tanzania and East Africa can get involved in something we’ve been on to for a while now – and open up a new market for SWE at the same time. And it’s working – Swala Tanzania shares are trading 400% up on the DES. The read through, taking into account % ownerships and asset allocation equates to a much higher valuation compared to that on the ASX. The past performance of this product is not and should not be taken as an indication of future performance. Caution should be exercised in assessing past performance. This product, like all other financial products, is subject to market forces and unpredictable events that may adversely affect future performance. Listing on the local stock exchange can only be a positive for relations with the Tanzanian government, especially crucial given bidding for the Eyasi license is starting to heat up. A big tick for the Tanzanian government is that awarding the licence to SWE will allow local Tanzanians the opportunity to retain ownership of the block in some way, through shares in SWE.

SWE driving hard toward 2015

2015 is going to be a big year for SWE right across its East African acreage. SWE has just announced a drill target at Block 12B plus made a firm commitment to drill an exploration well in 2015 with its JV partner Tullow. In Tanzania, SWE is gathering seismic at at its Pangani and Kilombero basin blocks so it can develop drilling targets for 2015. We should have results for both by the New Year. And in Zambia, SWE has formally won hydrocarbon exploration rights at Block 44 and will reprocess legacy data to determine the next step there. So across all assets, SWE is making moves and executing plans. We look forward to seeing details of the drilling plans for 12B in Kenya, results of the seismic surveys in Tanzania and updates on the reprocessing work in Zambia. In the coming months we should start to learn a fair bit more about SWE’s chances of finding the next big oil resource in East Africa.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.