In the Coming Days, this $8M Capped ASX Stock is Spudding a Well in an Oil Hot Spot

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

One $8M capped oil and gas producer and explorer is just a few days away from spudding a well offering near term production potential in a highly prolific onshore hydrocarbon region of Indonesia.

The low cost Amanah Timur-1 well is scheduled to spud around the 12 th December on an underexplored block that is on trend with major oil fields in the region.

The well should take around 15 days to complete, including testing time, so it won’t be long until results come through.

Site preparation is complete, the rig has been mobilised with rig up currently ongoing and with a recent $600k capital raise complete, this company will now be finding out a whole lot more about its two well-defined prospects.

The well is within the company’s South Block A PSC (40.7% net to this company), will be drilled to a depth of 530m, and will target sandstone reservoirs which have delivered over 600 mmbbl of oil, 2.2 tcf of gas, and 50 mmbbl condensate in close proximity.

Keep in mind that as this pre-1930 oil field produced from shallow depths, so there is a relatively high chance of striking commercial oil and there is every likelihood that hydrocarbons will be present in deeper undrilled sands as well.

Beyond the well to be drilled in the coming days, the company is also set to drill again in 2017, at Jerneh – which could prove to be a blockbuster gas deposit.

Jerneh is a prospective resource (P50) of 223 bcf of gas plus 5.3 mmbbl of condensate with a high side (P10) resource estimate of 760 bcf gas and 18 mmbbl condensate – meaning significant upside is on offer here for potential investors over the coming months, beyond the imminent well.

Over the past 18 months, this ASX company has restructured and minimised costs in a bid to ride out the oil market downturn, whilst building a portfolio that could transform the company from being a tiny Indonesian oil and gas explorer to become a prominent hydrocarbon producer in the region, in line with an anticipated industry pick up in 2017.

However, this company is still in its early stages and is some way from becoming a prominent hydrocarbon producer, as such investors should seek professional financial advice if considering this stock for their portfolio.

The focus for the company since its restructure has been to acquire either conventional producing or near term production assets, with a priority on gas, whilst still pursuing unconventional opportunities.

The company, capped at just AU$8M, has kept $1.75M in the bank, has just raised $600k and is therefore well-funded to progress its existing assets, including the current drilling of the Amanah Timur-1 well.

Furthermore, its Seram Project, which is producing oil under a PSC is already cash flow positive, bringing in AU$54,000 per month to the company.

The company’s assets are well situated, with two of its lead projects on trend where Exxon Mobil made its first major break in the region, with the 15tcf Arun gas field discovery that at its peak in 1994 produced 16.2 million tonnes of gas.

Indonesian domestic gas prices have maintained levels that continue to provide excellent returns on investment, particularly given capital and operating costs are at decade lows – so it looks like a great place for this stock to establish itself.

With energy demands increasing for both oil and gas in Indonesia, and with the current global climate buoyed by OPEC’s decision to cut oil production for the first time in eight years , this company is well located to supply the local market should its portfolio of prospects progress further.

Introducing...

![]()

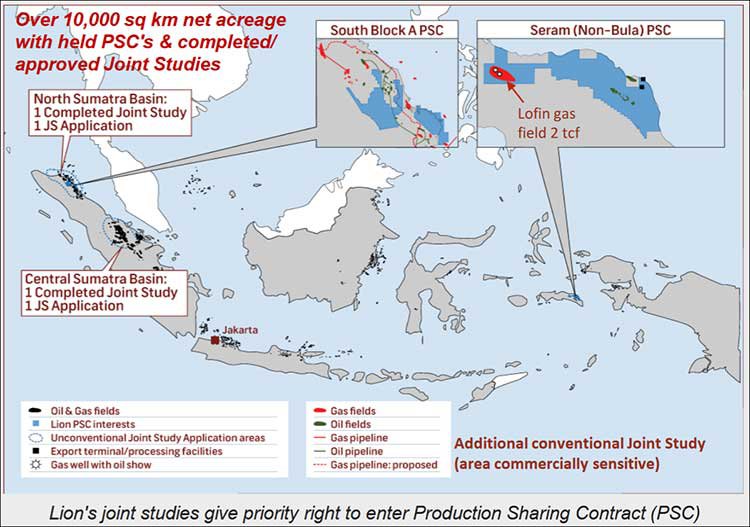

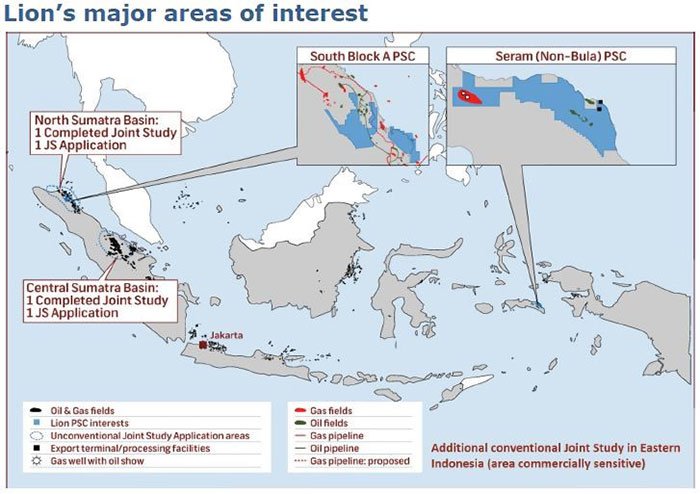

Lion Energy Limited (ASX:LIO) is an oil and gas producer and explorer with assets in key strategic locations within Indonesia. The company holds over 10,000 km 2 net acreage, located as shown on the map below:

The current economic climate in Indonesia is a positive one. It is currently the 16 th largest economy in the world and is predicted to move into 7 th position by 2030 with a GDP of US$862BN (AU$1163BN).

Yet as it stands, Australia does little business with its neighbour.

LIO looks to be bucking this trend, viewing Indonesia as an opportunity-rich country in which social and economic climates are positively aligning.

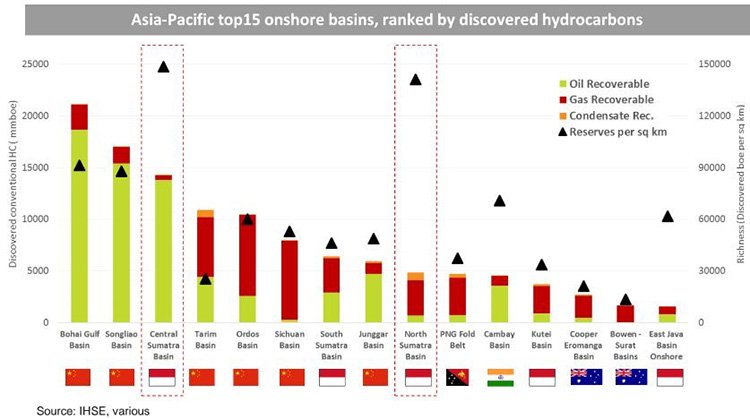

LIO has a mixture of conventional and unconventional projects located close to world renowned conventional oil and gas deposits in the most resource rich reserves per sq km in the Asia-Pacific region.

Indonesia, has in fact, been a hot spot for conventional oil and gas exploration for over 100 years.

And now the island nation is opening up for unconventional discoveries, which plays nicely into this fiscally disciplined company’s business strategy.

LIO is targeting conventional and unconventional prospects located within range of known abundant conventional oil and gas reserves and is set to aggressively advance its portfolio, with multiple short to mid-term catalysts on the horizon.

Since LIO repositioned itself at the beginning of 2014, the company has delivered on its promises, often ahead of schedule and under budget.

Here’s what the $8M capped LIO has been able to achieve up until now:

- In 2015, the Lofin-2 well was successful with ̴1300m gas column defined and certified Contingent Resource (2C) of 2.02 tcf (50bcf net to LIO)

- Successful Oseil development drilling, increasing production from an average 2600 bopd to ̴3600bopd with solid cash flow to Lion.

- South Block A PSC: 183km 2D seismic survey high-graded portfolio; LIO took the lead in technical work and the drilling of an attractive low risk oil well – which will be spudded in the coming days.

- It has converted Joint Study (JS) applications into PSC options, exploiting synergies between conventional and unconventional exploration. In fact two unconventional joint studies completed this year have ended with positive results and progress on other joint study applications over North and Central Sumatra Basins provide low cost options over large areas.

All the while, the company is continuously generating new portfolio opportunities.

The high quality and highly experienced LIO team, which is heavily invested in the company with 14% “skin in the game”, is largely the reason for the company’s success.

Board members of LIO either live in Indonesia or are there often, with a boots on the ground approach and understand how business is conducted in the country. They also have a deep network within the industry that can be leveraged when required.

Having weathered the downturn in oil prices, LIO is able to progress in a low-cost environment, giving investors the opportunity to take a position in a small capped stock with potentially rewarding oil and gas assets just as the oil price looks to mounting a recovery.

With a revenue stream already established and having just raised $600k, LIO may soon have a lot more to write home about if planned upcoming drilling is a success.

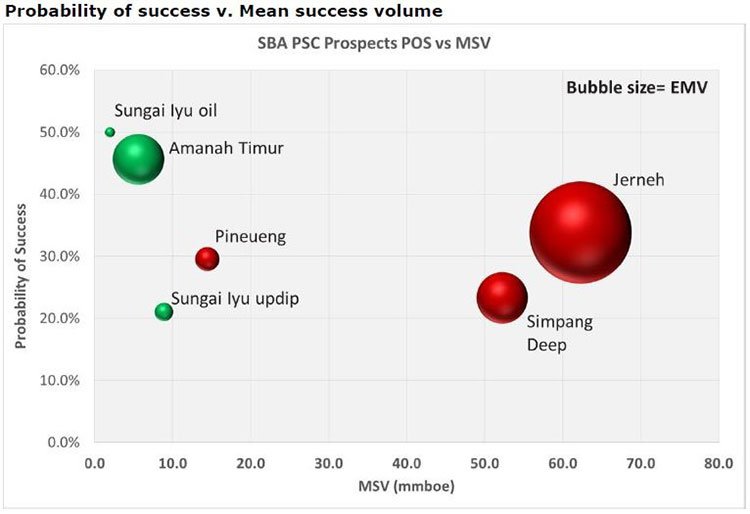

Here is a look at the company’s assets in the South Block A PSC exploration block in terms of project probability of success and possible size (oil in green, gas in red).

It is Amanah Timur that will be spudded in the company days, with Jerneh set for drilling in 2017.

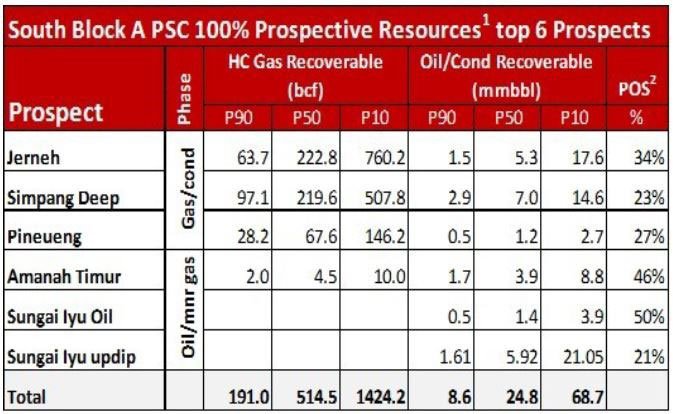

Here is a breakdown of prospective resources of each project in the South Block A PSC that LIO has a stake in:

Now, let’s look at the projects in more detail.

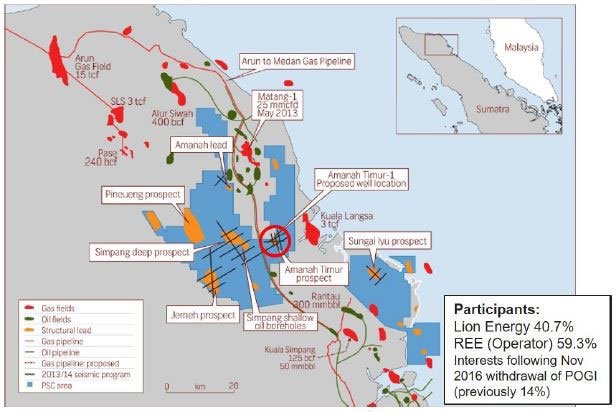

Near term drilling at Amanah Timur

Located in the north of the Indonesian island of Sumatra, LIO has identified a low-cost, low-risk oil opportunity known as the Amanah Timur prospect.

The area of South Block A that Amanah Timur sits in is one of the richest hydrocarbon regions in Indonesia based on reserves per square kilometre.

LIO holds a 40.7% interest in the South Block A PSC.

Seismic data hints at the presence of oil at shallow depths... and we should soon find out more once drilling begins.

Costs of the upcoming drilling program were significantly reduced from the original US$3.3M to $1.3M through further due diligence from the experienced management team.

LIO’s 40.7% share is only ~US$0.5mm and much of this has already been paid.

It should be noted that if initial drilling is successful at Amanah Timur, the company plans to accelerate production and cash flow. The development would be low-cost, as the project benefits from the well-established modern infrastructure already in place thus additional capital requirements should be relatively modest.

Also in place is the Arun LNG to Medan 400mmscfgd pipeline running only 100metres from the Amanah Timur project, making extraction of discovered gas resource a relatively inexpensive exercise.

Furthermore, there are good roads leading to the site, which is located only 6km from Langsa city which has a population of ~150,000.

Should drilling be a success, LIO plan to rapidly bring the project into production and cash flow.

Of course, like all oil exploration, drilling success is speculative at this stage and investors considering this stock for their portfolio should invest with caution.

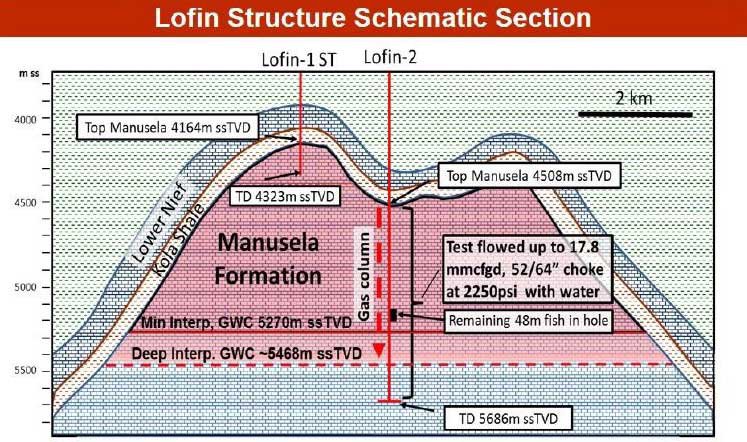

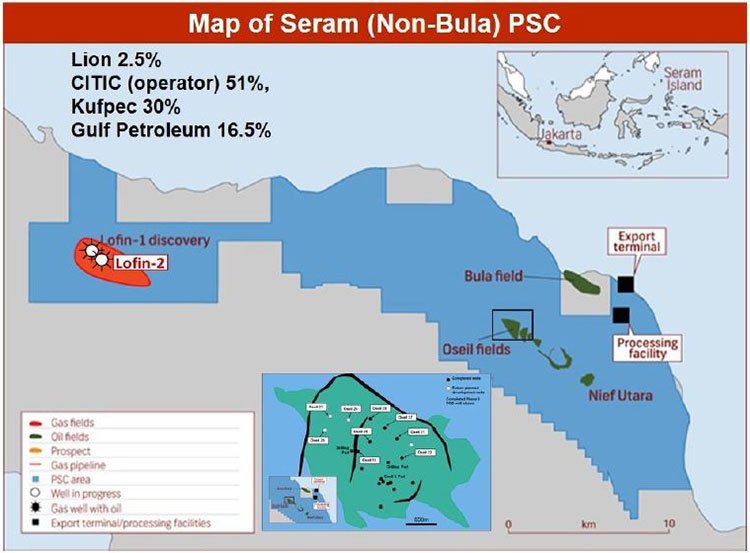

Lofin discovery is the largest in Indonesia in the past 10 years

LIO holds a 2.5% stake in this mega project that was discovered in 2012 and is believed to be the largest gas find in Indonesia in 10 years.

The Lofin field contains an enormous potential of 2tcf gas.

This was supported by a 2015 appraisal at Lofin-2 that confirmed a gas column of up to 1,300m in thickness.

Similarities can be drawn between Lofin and Sulawesi’s gas producing Donggi-Senoro LNG project which is located close by. The Donggi-Senoro LNG project involved the construction of a natural gas liquefaction plant near Luwuk in Central Sulawesi, Indonesia with a capacity of 2Mt of LNG and associated condensate a year.

The Donggi Senoro LNG plant began operations in June 2015 and supplied its first LNG cargo to Arun LNG receiving terminal in August 2015.

LIO believe that Lofin could be following a similar path, and if so would have a highly profitable asset on its hands.

Seram oil field producing revenues already

Lofin makes up part of the money-making Seram licence, which is currently producing around AU$135,000 per month in gross revenues each month for LIO, which generates net cash flow of $54,000 per month (assuming an oil price of US$38.)

Since production began in January 2003, the fields have produced over 15mm barrels, with the Oseil Field currently producing around 3,600 bopd.

Operating costs on the project have been substantially reduced in recent times from US$25 per barrel to only US$11.85 a barrel. This is well buffered from the realised Oseil crude current price of hovering at around US$40 a barrel.

These low production costs were achieved through a retendering of supply contracts, reduction in management wages and adjusting production output in order to reduce per barrel unit costs.

The current agreement sees LIO and its partners hold the rights to Seram up until 2019.

The partnership is well advanced in its application for an extension to secure the fields beyond this timeframe.

Upside potential with Jerneh gas find

Jerneh is a potential company-maker that if successful could transform LIO into a serious player in the undersupplied, high price, North Sumatra gas supply space.

LIO estimates a prospective resource (100%) at the P50 level of 223 bcf of gas plus 5.3 mmbbl of condensate with a P10 upside of 760 bcf gas and 18 mmbbl condensate.

The project has an estimated 34% chance of geologic success.

The Arun gas field is located in the North West where ExxonMobil made its big break and where Indonesia’s LNG plant produced a massive 16.2 million tons of gas in 1994.

Being along the trend of Arun and other major oil fields bodes well for LIO as the potential to strike a significant find sourced from the same prolific source rocks remains high.

LIO expects drilling at Jerneh to commence in 2017.

Future projects coming into frame mid-2017 and beyond

The high impact Simpang Deep prospect has an estimated P50 target of 220 bcf plus 7 mmbbl of condensate and represents an exciting follow up to success at Jerneh as it shares the same objectives formations.

Two unconventional joint studies have been completed and approved between leading Indonesian universities and LIO, where a large oil and gas potential has been identified in the Indonesian island of Sumatra.

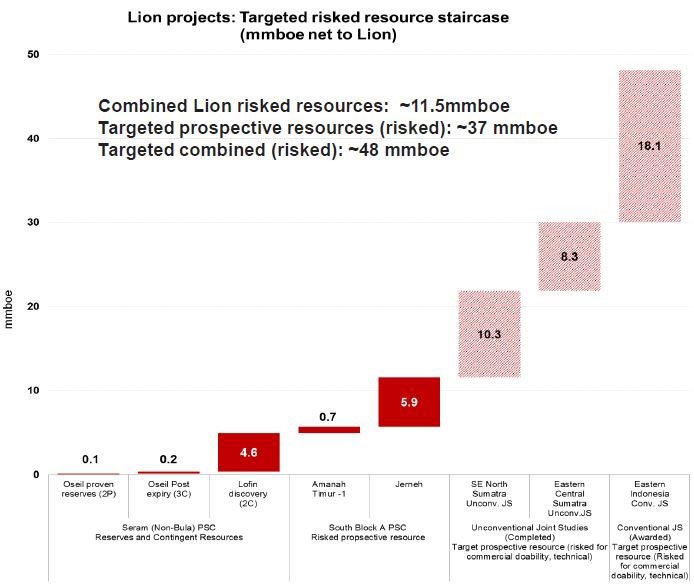

Here is a look at LIO’s potential resources (mmboe net to LIO):

It’s clear to see how LIO could be on the verge of a breakout over the coming months should drill results and follow-up prove successful on any number of its prospects.

With a skilled team in place managing LIO, potential opportunities should be maximised going forward.

Management team experienced throughout Indonesia

When operating in Indonesia it is important to have people there on the ground with a sound knowledge of the market and the people within it.

This is a major strength LIO possesses in terms of on-the-ground coverage in region, backed by a wealth of experience.

LIO Managing Director and CEO Kim Morrison has over 30 years’ experience as an exploration geologist, with a strong background in South East Asia, having had the company he co-founded KRX Energy incorporated into LIO in 2014.

Chairman of LIO, Russell Brimage has over 35 years’ experience in oil and gas upstream, and was the founder of Oilserv Australia Ltd. A successful oil testing company providing a range of services to some of the biggest oil players in the Australia.

Principal Advisor Sammy Hamzah has played a pivotal role at LIO with his connections inside Indonesia. Sammy is an Indonesian national and has a great understanding and respect within the local industry.

Other members on the board have extensive experience operating in Indonesia, including Non-Executive Directors Tom Soulsby and Chris Newton who are the CEO and CFO respectively of Indonesian owned PT Energi Mega Persada. Persada is a well-established independent oil and gas company headquartered in Jarkata, Indonesia, with a market cap of approximately US$164 million.

Finance director Stuart Smith has over 20 years’ experience in the energy sector as a chartered accountant, having held leadership roles in the industry over the years including time as the head of oil and gas research for Merrill Lynch in the Asia Pacific region (including Indonesia).

Indonesian government supporting industry as energy demand skyrockets

With an oil industry over a century old, Indonesia relies heavily on its oil sector for its economic strength, hence is well supported by the government.

President Joko Widodo is focused on developing local infrastructure with a development plan costing US$440 billion between 2011-2025, of which US$196 billion has been assigned to roads, railways, ports and power plants.

Indonesia itself is the world’s 16 th largest economy, with an estimated GDP output of US$862 billion, and is expected to be the 7 th largest economy in the world by 2023.

There are currently 255 million people living in Indonesia, making it the fourth most populated country in the world.

This growing population has a thirst for oil and gas to drive its energy needs going forward, with electricity growth forecast to rise 8.7% per annum over the following decade.

So great is the demand that within the next five years Indonesia will become a net oil and gas importer.

Whilst every country contains an element of sovereign risk, Indonesia offers high return potential with relatively low risk.

With 3.3% inflation, unemployment rate of 5.5% and debt/GDP at 27%, you could even say that on many metrics the Indonesian economy is healthier than Australia.

All this is positive news for LIO seeking to operate in Indonesia’s well established oil industry and target the unconventional market, which is still in its infancy.

With oil supply decreasing and demand increasing, energy prices are on the rise.

This rise has been further strengthened by the OPEC decision to cut oil production for the first time in eight years. That decision sent crude oil prices soaring.

https://www.bloomberg.com/news/articles/2016-11-30/opec-decision-day-as-ministers-meet-to-salvage-deal-on-oil-cuts

If LIO prospects make it through to production phase, the company could see higher prices leading to increased margins.Upcoming catalysts for LIO

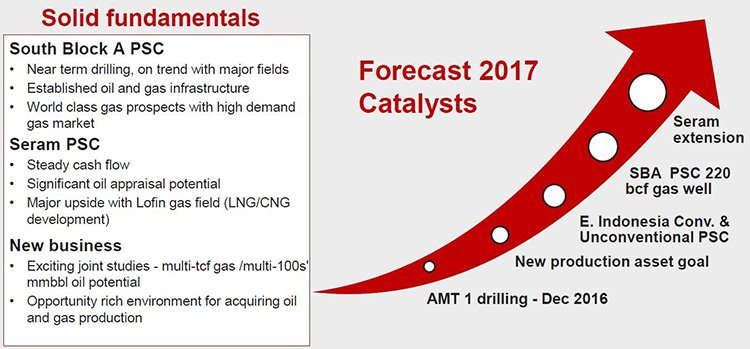

LIO has exposure to a number of significant near to mid-term catalysts that could more than interest the market.

Drilling is set to take place in the coming days at Amanah Timur, which is said to have a 46% chance of success.

The constant stream of around US$40k each month in net revenues keeps ticking away.

In the mid-term, drilling at Jerneh in 2017 could prove to be a blockbuster gas deposit.

Should LIO find what they are hoping at Jerneh we could see the company receive a rapid rerating from the market.

Of course any re-rating would require the company to meet all its objectives and the markets to treat it favourably. This may or may not occur and investors considering this stock should seek professional financial advice before making an investment decision.

The two completed studies in oil rich Sumatran Indonesia will likely come into frame later in 2017, with a conventional study in Eastern Indonesia with huge upside currently in progress.

A further two unconventional studies have been submitted. In total the four unconventional studies lodged by LIO cover over 17,334km.

The joint studies ensure LIO receives first bite at the cherry should they choose to progress on the areas studied.

With the oil price forming a bottom and LIO just days away from news flow with regards to drilling, this could be an opportunity to get into an emerging oil explorer at the bottom of the price cycle.

And with mergers and acquisitions coming back into the market, LIO may seek to continue to acquire prospects or find itself on the end of a buyout offer.

Whatever happens in the coming months, it looks to be positive for this well-placed producer and explorer.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.