AOW Could Double its Oil Reserves With Latest Acquisition

Published 08-NOV-2017 16:39 P.M.

|

9 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

With a significant war chest in its possession, American Patriot (ASX:AOW) is quickstepping towards its long-term goal to build a significant producing business, reaching 500 bopd by year’s end and 3000 BOPD by the end of 2019.

Just this week, AOW signed a Letter of Intent (LOI) to acquire additional conventional oil and gas assets in East Texas. The acquisition would effectively double its reserves to 2.1 million barrels of oil equivalent.

It hasn’t been long since we caught up with AOW.

Back in mid-September when we last reported on AOW’s progress, it had embarked on its intended acquisition spree, picking up assets that had significant implications for the company.

The acquisition gave AOW 50 barrels of oil per day with minimal rework that is set increase to over 150bopd. It also delivered 300,000 barrels proven oil reserves and the potential for USD$11m revenue – a move that kept AOW on track to deliver its first revenues by the end of 2017.

The acquisition played into AOW’s mission to acquire distressed assets with viable oil production resources for cents on the dollar.

It is cherry picking the best assets across the US as it continues an aggressive acquisition strategy by restarting production at shut wells, rather than starting new ones.

The company, however, is still an early stage play and as such investors should seek professional financial advice if considering this stock for their portfolio.

The latest acquisition fits its strategy nicely.

It consists of 37 barrels of oil per day and 440 mcfd of gas production (110 boepd) with plenty of upside potential and contains 1,100,000 barrels of oil equivalent proven oil and gas 1P reserves certified by independent reports.

Importantly, these assets could generate US$ 20 million of revenue.

AOW sees the acquisition as a step change in the transformation of the junior into a significant production company.

With that in mind, let’s look into the latest acquisition news from AOW.

![]()

OTC QB:ANPOF:US

American Patriot (ASX:AOW) has stepped up the pace on its acquisition strategy.

Since August this year it has been aggressively chasing distressed assets with low production costs on its mission to produce a conventional oil business that will produce over 3000 barrels of oil per day by 2019.

For a quick recap of recent acquisitions, you can read our reports including AOW Acquires Producing Oil & Gas Reserves: More Acquisitions to Come and AOW Swoops on Distressed Texan Oil Seller: Proven Oil Reserves Secured .

The acquisitions reported in the articles above have paved the way for AOW’s latest piece of the puzzle and what looks to be its biggest coup yet, with even bigger deals – almost five times this latest acquisition – on the horizon as well.

AOW doubles proven reserves

AOW has just completed its fourth acquisition of what it believes is many attractive new targets to come.

On its way to building one of the best recognised producing conventional oil businesses, AOW is now in the throes of completing its largest transaction to date – doubling its reserve base and production potential in the one transaction.

The latest assets consist of 37 barrels of oil a day and mcfd of gas production (110 barrels of oil equivalent per day) with significant upside potential.

The asset contains 1.1 million barrels of oil equivalent proven oil and gas 1P reserves certified by independent reserve reports. These reserves have been acquired for US$2.5 million and are estimated to have the potential to generate USD$20 million revenue over a period of time.

This is a speculative figure at this stage, so investors should approach any investment decision in this stock with caution and look at all publically available information before making an investment decision.

$20 million is a solid number and when combined with other assets and could put AOW in an enviable revenue position.

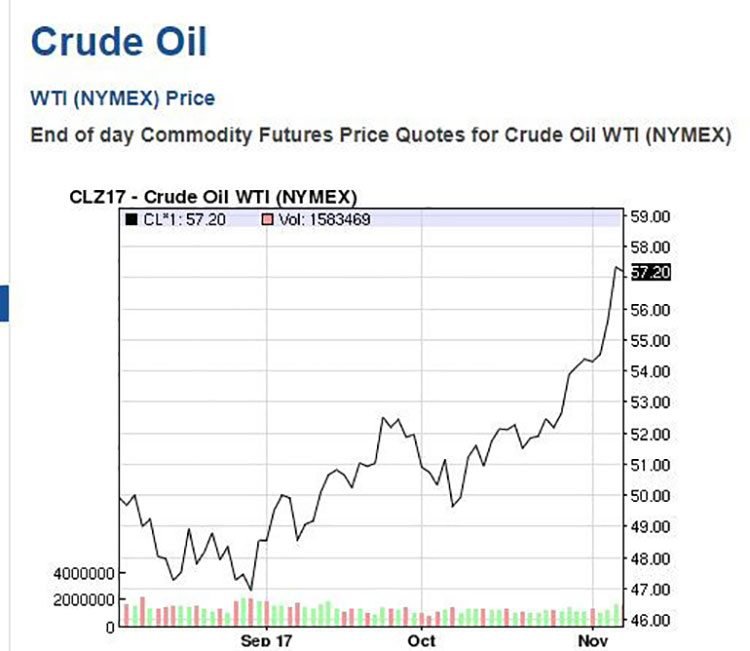

The reserve study had been conservatively valued at US$50/bbl oil prices at a time when the market price is US$57/bbl and OPEC is eyeing $70 – more on that later.

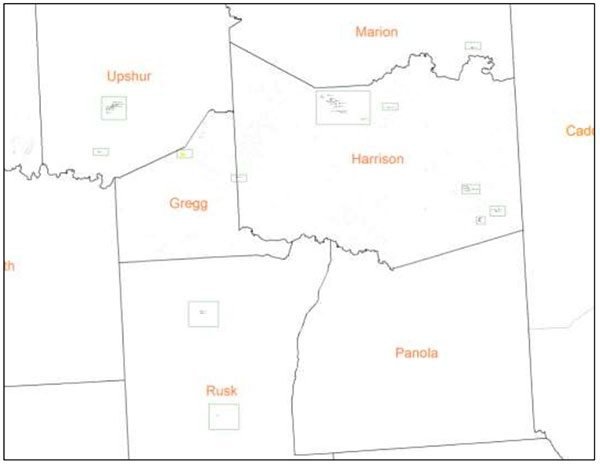

The assets have been acquired from a number of private oil and gas companies. Here is a look at the acquired fields located in Harrison, Gregg, Rusk and Upshur Counties, Texas:

There are over 38 producing wells over 43 leases with an average net revenue interest (NRI) of 76 per cent. Estimated reserves are 400,000 bbls oil and 4 bcf gas.

AOW has already completed an independent reserve report and full engineering study on the assets. There is further due diligence to come including land title and environmental work, with the transaction due to close in early December, just a few weeks from now. Importantly its financial backers have also independently completed due diligence on the assets and its own engineering analysis supports the reserve base.

In line with AOW’s strategy, operating costs in this region are approximately $23/bbl, so the wells are economic down to a low oil price and looking very profitable at the current price of oil.

Like its other recently acquired assets, there is minimal work to be done here with infrastructure including pump jacks, tanks and batteries in place, pointing to minimal workover expenditure to increase production in the field.

Ready access to market through gas pipeline and delivery to nearby refineries is also highly beneficial for AOW.

Combined with other assets, AOW is well on track to achieve 500 boepd by the end of the year, which is only six weeks away, with two million barrels of proven oil and gas reserves certified by independent reserve reports. These assets are expected to generate over $50 million revenue at current oil prices over time.

It will be even better if oil prices continue to rise as expected.

Oil on the up

AOW would be well aware of rising oil prices.

Here’s a look at where the oil price currently sits:

OPEC expects this trend to continue.

We are just three weeks away from OPEC’s November summit and all indications are that some oilers are already thinking that $70 is a fair price for oil .

With that information in the bag, it looks as though AOW’s low cost gameplan is already paying off.

Recapping its acquisitions

As we mentioned earlier, the acquisition spree began in August when AOW did deals for conventional oil and gas assets in south Texas.

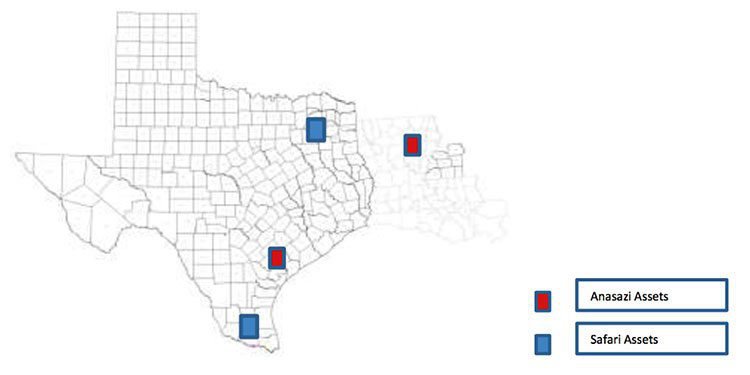

Ansazi & Safari

Thus far, AOW has successfully completed due diligence and signed Purchase and Sale agreements and Asset assignments covering transactions with Safari Oil and Gas Production Inc. and Anasazi New Ventures corporation to acquire 100% of these companies’ assets.

Here’s a look at the acreage:

It was a great start for AOW, giving it conventional oil and gas assets in the southern region of Texas, consisting of 285 boepd/900,000 barrels of oil equivalent 1P reserves certified by independent reserve reports.

The assets are expected to generate more than US$2 million in annual net cash flow at US$47 a barrel oil prices. There’s that low oil price again.

The purchase includes over 30 well bores of existing conventional production. Management also sees the potential to grow production significantly by restarting shut in production and workover/behind pipe potential on the existing wells. It is of the view that this can be done cost effectively, maintaining the economic viability of the wells.

The transactions in Tranche 1 include oil and gas production of 170boepd (barrels of oil equivalent per day) and 1P proven reserves of 300 mboe supported by an independent reserve report.

The assets in tranche 1 are forecast to generate USD$1 million of annual cash flow net to AOW.

The assets included in Tranche 2 are expected to more than double the production and reserve base acquired in Tranche 1, delivering an additional 120 boepd and 1P proven reserves of 700mboe.

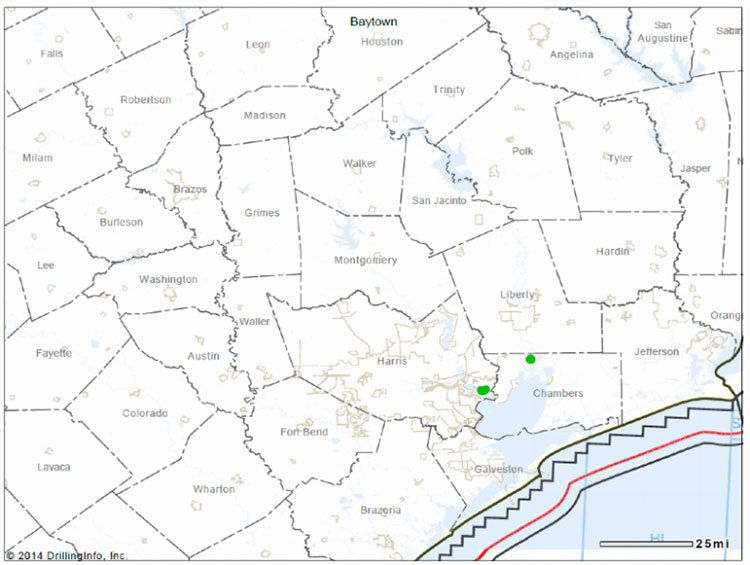

Lost Lake & Goose Creek

Following its August acquisition, AOW backed up with the acquisitions of Lost Lake/Goose Creek including 50 bopd shut in and 1P proven reserves of 300 mboe.

The assets were acquired out of Chapter 11 bankruptcy from major lender Solstice Capital LLC at the Bankruptcy court in Houston.

The Lost Lake and Goose Creek Oil fields are located in the Harris and Chambers counties, Texas as seen below:

The assets consist of 65 oil wells covering approximately 340 leasehold acres HBP at 100% GWI/average 75-81% NRI in Harris and Chambers counties Texas.

They also consist of 50 barrels of oil per day of conventional production with considerable upside and contain 300,000 barrels proven oil and gas (mboe) 1P reserves certified by independent reserve reports, estimated to generated US$11 million revenue with a PV10 value of $USD3 million acquired for US$430k.

AOW is looking to quickly restart the 50bopd shut-in production at a low or minimal cost and generate immediate cash flow. The upside may also be readily achievable with workovers at low cost, which will double or triple production in the next 12 months.

This is a great example of AOW’s strategy in action: significant reserve potential and upside which the previous owner was unable to exploit.

Money in the bank

These acquisitions are backed by the completion of an oversubscribed $1.3 million capital raise , with funds going towards further acquisitions.

This was complemented by the execution of a debt facility term sheet for increased facility size of up to $40 million.

AOW announced the debt facility in late September with a major New York based institutional investor. The paperwork is still to be completed, however this is expected to be finalised in approximately a month.

The increased facility will enable AOW to undertake further acquisitions in the next 12 months that could help to grow production, cash flow and reserves – all leading to a stream of potentially positive news flow.

In the pipeline

By all reports, AOW has a solid pipeline of deals in the works and is now emerging as a noteworthy US oil and gas production company with an immediate and growing cash flow and reserve base in Texas, fully supported by its US-based funders.

Yet this remains a speculative stock and investors should seek professional financial advice if considering this stock for their portfolio.

It is now looking to further accelerate its production growth and reserves, which will enable AOW to deliver on the strategy of aggressively building a producing conventional oil business with well over 1000 barrels of oil per day production in 2018.

AOW is now listed on both the US OTC QB market and the ASX, and will also be looking to up-list to a significant US stock exchange in the next 12 months.

If it can achieve all its aims, this $8 million capped minnow with major ambitions could considerably turn its tiny market cap into something as potentially as big as Texas.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.